ERP Integration for TDS Reconciliation: Guide for Indian Enterprises (FY 2026–27)

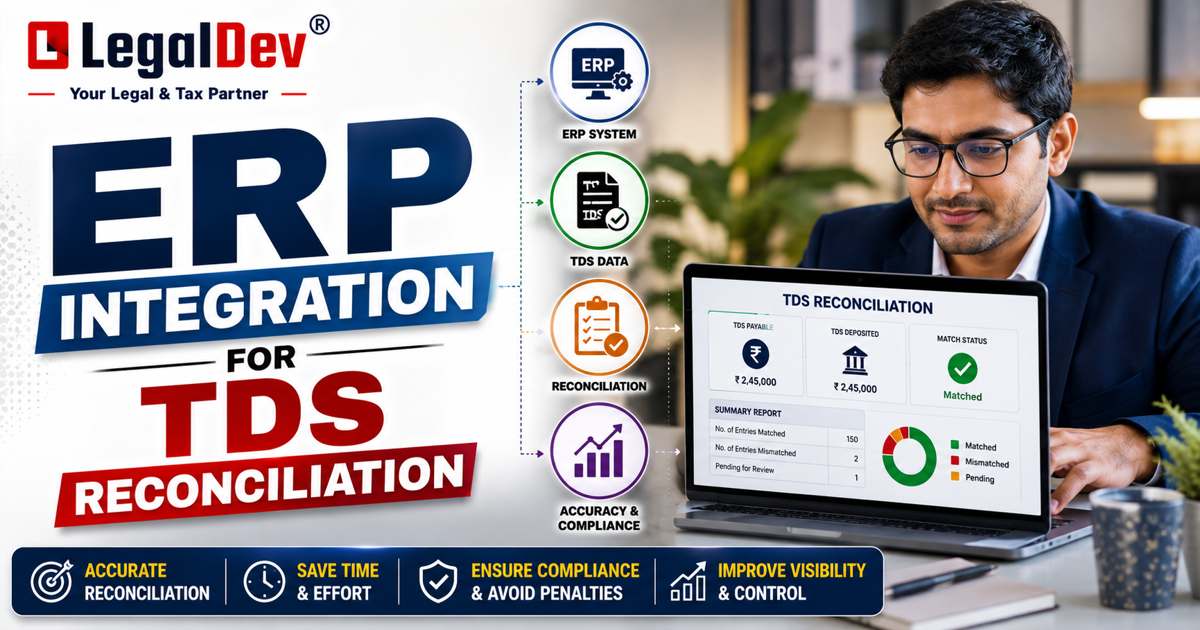

Indian businesses processing high-volume vendor payments know the pain TDS entries sitting in the ERP on one side, Form 26AS showing something different on the other, and a quarterly deadline closing in fast. ERP integration for TDS reconciliation was built specifically to close that gap. Instead of manually exporting CSVs, comparing spreadsheets, and chasing mismatches across TRACES and OLTAS, it creates a continuous, validated data flow between your general ledger and the government portals.

And with the Income Tax Act 2025 in force from 1 April 2026 bringing new 4-digit payment codes, renamed return forms, and a restructured TDS framework the cost of not having this integration in place just got measurably higher.

A few things to know before we get into the how:

-

Manual TDS reconciliation at scale almost always produces errors PAN mismatches, wrong Challan Identification Numbers, incorrect Assessment Year tagging. Each one carries a cost.

-

Automated three-way matching across books, OLTAS challans, and Form 26AS/AIS reduces reconciliation time from days to hours.

-

The new Income Tax Act 2025 requires all ERP systems to use 4-digit payment codes (1001–1092) replacing legacy section numbers like 194C and 194J effective from the first payment made in FY 2026–27.

-

Form 26AS itself transitions to Form 168 from Tax Year 2026–27, integrating AIS data into a single consolidated statement.

What Is ERP Integration for TDS Reconciliation?

TDS reconciliation means matching tax deducted at source across three distinct data sources:

|

Source

|

What It Contains

|

|

ERP / Books of Accounts

|

TDS deducted, challans deposited, vendor PAN, section codes (now payment codes)

|

|

TRACES Portal

|

Filed returns (now Forms 138/140/143/144), challan status, Form 130/131 data

|

|

Form 26AS / AIS (Form 168 from TY 2026-27)

|

Consolidated tax credit as seen by the deductee

|

Any mismatch across these three sources can result in the deductee losing TDS credit or facing a tax demand. The deductor meanwhile sits exposed to interest, expense disallowance, and late filing fees all now governed by the Income Tax Act, 2025.

ERP integration removes the manual layer entirely. No CSV exports. No quarterly fire-fighting. Just a clean data pipeline from your general ledger to government portals running continuously, not just at quarter-end.

Why Manual TDS Reconciliation Breaks Down

The errors are predictable. The damage is not.

|

Challenge

|

Business Impact

|

|

PAN/TAN errors in returns

|

Credit not reflected in 26AS; deductee disputes arise

|

|

Wrong Assessment Year tagged

|

TDS reflected in wrong year; ITR filing mismatches

|

|

Challan CIN mismatch

|

Tax payment not linked to TDS statement on TRACES

|

|

Multi-TAN reconciliation

|

No consolidated view; separate manual runs per TAN

|

|

Section misclassification (194J vs 194C)

|

Short deduction, expense disallowance risk

|

|

New 4-digit payment codes from April 2026

|

Old section codes trigger FVU validation errors filings rejected

|

|

March deductions processed in April

|

Quarter-end mismatches with no automated resolution path

|

That last point about payment codes is worth pausing on. If your ERP still carries 194C or 194J as the section reference for April 2026 transactions, those returns will fail FVU validation on TRACES. The Income Tax portal simply will not accept them.

Step-by-Step ERP Integration for TDS Reconciliation

Step 1: Map ERP GL Accounts to TRACES Fields

Start by segmenting TDS GL accounts TAN-wise and linking vendor PAN masters across your ERP. Then update every section code to the new 4-digit payment codes under the Income Tax Act, 2025.

Under the new Act, all TDS provisions consolidate under Section 392 (salary and EPF), Section 393 (all other resident and non-resident payments), and Section 394 (TCS). What was 194C is now Section 393 with payment code 1023 or 1024. What was 194J maps to Section 393 with payment code 1026. These codes are mandatory for FY 2026–27 your ERP master data must reflect this before the first challan of the new financial year.

Step 2: Automate Challan Pull from OLTAS

Integrate with OLTAS via API or SFTP to match each Challan Identification Number against your books in real time. The goal is straightforward: unmatched or failed challans get flagged before the quarterly return is filed, not after the deductee raises a credit dispute.

Manual OLTAS matching across 500+ vendors is where most finance teams lose days every quarter. An automated pull eliminates that entirely.

Step 3: Import TDS Returns from TRACES

Set up automated import of filed TDS return data from TRACES now using Forms 138 (salary), 140 (non-salary residents), 143 (non-residents), and 144 (TCS) under the new Act to build the three-way match: books → challan → return.

This three-way match is the core of the reconciliation engine. Without automating the import, you are matching by hand, and that means errors. It also means you are always a step behind.

Step 4: Pull and Reconcile Form 26AS / AIS (Now Form 168)

Automate periodic pulls of Form 26AS and AIS from the Income Tax Portal minimum quarterly, monthly recommended for high-value vendor portfolios.

From Tax Year 2026–27, Form 26AS is replaced by Form 168, which integrates AIS data into a consolidated statement. TRACES section code fields in Form 168 will show new Section 393 sub-clauses rather than legacy section numbers any reconciliation engine not updated for this format will produce misclassified matches and create new problems rather than solving old ones.

The engine should classify each entry as:

-

Matched — Exact or within defined tolerance (±₹1 is the standard)

-

Suggested — System-defined tolerance match requiring review

-

Unmatched — No corresponding entry on either side

-

Missing — PAN or TAN absent in Form 168

Lower Deduction Certificate limits for high-value vendors should apply automatically at this stage not as a manual check added at quarter-end.

Step 5: Resolve Discrepancies

|

Mismatch Type

|

Resolution

|

|

TDS credit less than deducted

|

Deductor files correction return on TRACES

|

|

Wrong Assessment Year tagged

|

Correction in return for correct assessment year

|

|

Challan CIN mismatch

|

Challan correction on TRACES portal

|

|

PAN error

|

Correct deductee PAN in TDS return

|

|

Section misclassification

|

File correction statement with correct payment code

|

|

Cross-year reconciliation (old 194C vs new code 1023)

|

Dual-mode matching treat paired codes as equivalent during transition

|

That cross-year reconciliation requirement is new for FY 2026–27. Historical transactions carry old section codes; new transactions carry Section 393 payment codes. Any reconciliation platform handling enterprise TDS across this transition period needs dual-code matching logic built in most legacy tools do not have it.

Step 6: Generate FVU and File

Once the reconciliation is clean, generate FVU files from the integrated platform and submit to TRACES. Bulk PAN verification against TRACES records should run automatically before submission rejections from PAN mismatches at this stage are entirely avoidable.

Step 7: Distribute TDS Certificates

Automate generation and bulk distribution of TDS certificates to deductees. Under the Income Tax Act, 2025, these are now Form 130 (replacing Form 16 for salary) and Form 131 (replacing Form 16A for non-salary). The renaming is mandatory certificates issued under old form numbers for FY 2026–27 transactions will not be compliant.

Benefits of ERP Integration for TDS Reconciliation in India

|

Benefit

|

What It Means in Practice

|

|

No manual data extraction

|

Direct GL / API feed; no CSV exports or imports

|

|

Continuous reconciliation

|

Monthly Form 168 matching vs. year-end scramble

|

|

Multi-TAN consolidated view

|

Single dashboard across all deductor entities

|

|

Proactive notice prevention

|

Errors caught before filing not after scrutiny notices arrive

|

|

Full audit trail

|

Every reconciliation run, correction, and filing logged

|

|

FY 2026–27 ready

|

New payment codes 1001–1092, renamed forms pre-mapped

|

The compliance readiness row is the one that has become urgent. Any enterprise running legacy ERP TDS configurations into FY 2026–27 is not just at risk of FVU errors. It is at risk of deductee credit disputes, correction return filings under time pressure, and downstream ITR mismatches all of which are preventable.

Real-World TDS Reconciliation Scenarios

Scenario 1: Manufacturing (SAP ECC, 500+ Vendors, 3 TANs)

Quarterly reconciliation across three TANs was taking over ten person-days, with 194C/194J misclassifications surfacing only at year-end. Post-ERP integration: GL data auto-pulled, section codes updated to new 4-digit payment codes, correction FVUs generated in hours.

Scenario 2: IT Services (Oracle Fusion, Multi-Entity)

AIS flagged a TDS shortfall from a major client. Locating the Challan CIN error manually required cross-referencing three assessment years of records. Post-integration: automated AIS import identified the mismatch in minutes, pinpointed the challan, and generated the correction return in the same workflow.

Both scenarios share the same root cause reconciliation was a manual, periodic event rather than a continuous automated control. The integration does not just speed things up. It changes what gets caught and when.

How to Choose the Right TDS Reconciliation Software for ERPs

Not every platform advertising "TDS automation" handles the complexity that enterprise workflows actually generate. The features that matter:

-

Native ERP connectors — SAP S/4HANA, SAP ECC, Oracle NetSuite, MS Dynamics, Tally, 100+ others; direct GL ingestion, no manual upload

-

TRACES integration — auto-import of filed return data; bulk PAN verification before FVU submission

-

Form 26AS / AIS / Form 168 reconciliation — vendor-wise matched, suggested, and unmatched classification with configurable tolerance

-

Multi-TAN dashboard — consolidated view across all deductor entities, not separate runs per TAN

-

FVU generation and filing — end-to-end from GL to submitted return in one workflow

-

FY 2026–27 readiness — payment codes 1001–1092 and renamed forms pre-configured; dual-mode cross-era matching for the transition period

-

LDC management — automatic application of Lower Deduction Certificate limits for high-value vendor payments

Legaldev Compliance Cloud: ERP Integration for TDS Reconciliation

Legaldev's GL-Stream technology eliminates the manual transformation layer by streaming data directly from the general ledger. TDS GL accounts, trial balance, deductions, and corrections run in a single automated workflow with 200+ system-led validations catching ERP accounting gaps before they reach the filing layer.

|

Feature

|

Capability

|

|

GL-Stream Technology

|

Direct general ledger ingestion no CSV, no manual upload

|

|

200+ System-Led Validations

|

Catches ERP accounting gaps before the filing layer

|

|

TRACES Integration

|

Auto-imports TDS return files; bulk PAN verification included

|

|

26AS / AIS / Form 168 Reconciliation

|

Monthly or quarterly; vendor-wise matched/unmatched classification

|

|

Multi-TAN Dashboard

|

Consolidated view across all TANs and deductor entities

|

|

FVU Generation & Filing

|

GL data to submitted return in one workflow

|

|

ERP Compatibility

|

SAP S/4HANA, SAP ECC, Oracle NetSuite, MS Dynamics, Tally, 100+ others

|

|

TDS Certificate Distribution

|

Automated Form 130/131 bulk issuance

|

|

FY 2026–27 Ready

|

New payment codes 1001–1092, renamed forms pre-configured

|

Over 500 ERP integrations completed SAP S/4HANA/ECC, Oracle NetSuite, MS Dynamics/Navision, Tally, and 100+ others with data ingestion via APIs, SFTP, or templates.

The FY 2026–27 Transition: What Needs to Happen in Your ERP Before the First April Challan

This is where most enterprises underestimate the scope of work.

The Income Tax Act, 1961 which governed every TDS transaction in India for over six decades stood repealed on 31 March 2026. From 1 April 2026, the Income Tax Act, 2025 applies to every new payment and credit. That means:

-

Every ERP payment master still referencing 194C, 194J, 194H, or 194I needs updating before the first payment of FY 2026–27

-

Vendor masters need annotating with the correct 4-digit payment code (1001–1092)

-

Reconciliation configurations need dual-mode matching logic — cross-year cases involving both old codes and new codes will continue for at least two financial years

-

TDS return form templates need updating to Forms 138, 140, 143, and 144

-

TDS certificate templates need updating to Forms 130 and 131

-

Form 26AS references throughout the system need updating for Form 168

Platforms with these changes pre-mapped requiring no client-side configuration are the ones that enterprises will not be scrambling to fix after the first quarterly filing produces errors.

For Indian enterprises managing TDS at scale across multiple ERPs and TANs, the Income Tax Act, 2025 has made ERP integration for TDS reconciliation a compliance necessity rather than an operational convenience. Delayed implementation now carries direct legal and financial exposure. The reconciliation workflow that worked in FY 2025–26 will generate errors in FY 2026–27 if the underlying ERP configurations have not been updated. That is not a forecast it is how FVU validation works.

FAQs

Q: How does ERP integration help in TDS reconciliation?

A: Once integrated, your ERP streams GL data directly to the reconciliation engine automating challan matching against OLTAS, PAN validation, Form 26AS / Form 168 comparison, and FVU generation for TRACES filing. Reconciliation time that typically runs 7–10 days per quarter for large vendor bases drops to hours. The bigger gain is that errors are caught before filing, not after scrutiny notices arrive.

Q: What is challan reconciliation in TDS, and how does ERP integration help?

A: Challan reconciliation matches each Challan Identification Number from your tax deposit in OLTAS against your books and filed TDS return. If the CIN in your books does not match what TRACES shows, the deductee's credit does not appear in Form 26AS or Form 168. ERP integration automates this three-way match books, challan, and return and flags unmatched challans before the quarterly return is submitted, not after the deductee raises a credit dispute.

Q: What are the new TDS payment codes under the Income Tax Act 2025?

A: From 1 April 2026, all TDS/TCS transactions must use 4-digit numeric payment codes in the range 1001–1092, replacing legacy section numbers like 194C, 194J, 194H, and 194I. These codes fall under Section 392 (salary), Section 393 (all other resident and non-resident payments), and Section 394 (TCS). Any ERP or TDS software still using old section codes for FY 2026–27 transactions will fail FVU validation on TRACES.

Q: What happens to Form 26AS under the Income Tax Act 2025?

A: From Tax Year 2026–27, Form 26AS is replaced by Form 168, which integrates Annual Information Statement data into a single consolidated tax credit statement. TRACES section code fields in Form 168 show new Section 393 sub-clauses rather than legacy section numbers. Any automated reconciliation platform needs to handle both formats simultaneously old codes for FY 2025–26 historical transactions, new codes for FY 2026–27 onwards.

Q: What features should enterprises look for in TDS reconciliation software for FY 2026-27?

A: The non-negotiables are native ERP connectors (SAP, Oracle, Tally, and others), direct TRACES integration with auto-import of return data, Form 26AS / AIS / Form 168 vendor-wise reconciliation, multi-TAN consolidated management, bulk PAN verification before FVU submission, and FY 2026–27 readiness meaning new payment codes 1001–1092 pre-mapped, renamed forms (130/131/138/140/168) pre-configured, and dual-mode cross-era matching for the transition period.

Q: How does AIS data help in TDS reconciliation for Indian enterprises?

A: AIS aggregates TDS credit across all deductors with more granular transaction-level detail than Form 26AS historically provided. Automating AIS pulls lets finance teams identify missing credits early before ITR filing deadlines and raise correction requests with deductors while there is still time to act. That said, the Income Tax Department has clarified that Form 168 (formerly Form 26AS) remains the authoritative source for TDS credit claims; AIS is for completeness verification.

Q: Can TDS reconciliation software handle multiple TANs for the same enterprise?

A: Yes, and this is one of the primary reasons enterprises move to integrated platforms. A multi-TAN dashboard consolidates challan tracking, return filing, reconciliation runs, and TDS certificate distribution across all deductor entities in a single interface. Without this, each TAN requires a separate manual workflow multiplying effort and error surface proportionally.

Q: What is the risk of not updating ERP section codes before April 2026 TDS filings?

A: Returns filed using legacy section codes for transactions dated from 1 April 2026 onwards will fail FVU validation on TRACES and be rejected. Downstream, deductees will not see their TDS credit in Form 168 until a corrected return is filed — triggering credit disputes, ITR mismatches, and demand notices, with interest accruing throughout the correction period.

Q: What is the difference between Form 26AS and AIS for TDS reconciliation purposes?

A: Form 26AS (now transitioning to Form 168 from Tax Year 2026–27) shows TDS and TCS credits, advance tax, and self-assessment tax the records directly relevant to TDS credit claims. AIS is broader: it captures 46 categories of financial information including dividend income, securities transactions, and foreign remittances. For TDS reconciliation specifically, Form 168 is the authoritative credit-level document. AIS is used for income completeness checks rather than credit verification.

Q: How long does ERP integration for TDS reconciliation take to implement?

A: Most enterprise deployments complete in 2–4 weeks for standard ERP connectors (SAP, Oracle, Tally) with clean vendor master data. The main variables are data quality in existing PAN/TAN masters, number of TANs, and whether historical reconciliation data needs importing. Platforms with pre-built connectors for 100+ ERPs and SFTP/API-based GL ingestion avoid the configuration work that extends timelines.