Many investors who build long-term portfolios tend to focus on past performance metrics (the things that have happened within the market in the past) and neglect to understand how the value of a fund is actually derived. The term Net Asset Value (NAV) is often used in these discussions regarding the design of a portfolio.

Many investors who build long-term portfolios tend to focus on past performance metrics (the things that have happened within the market in the past) and neglect to understand how the value of a fund is actually derived. The term Net Asset Value (NAV) is often used in these discussions regarding the design of a portfolio.

When establishing a wealth management plan, it is important to fully understand how the NAV calculation works and how it relates to the generation of long-term wealth; however, there are many principals have a misunderstanding of it and as a result, choose a mutual fund solely based on its share price (e.g., “cheap versus expensive”) rather than whether or not it aligns with their desired outcome for capital growth.

The purpose of this guide is to present the relevant information regarding NAV in layman’s terms, including what it is, how asset managers determine it on a daily basis, and whether or not the concept of NAV should have an impact on the investment decisions made by today’s investors based on regulatory standards.

What is NAV?

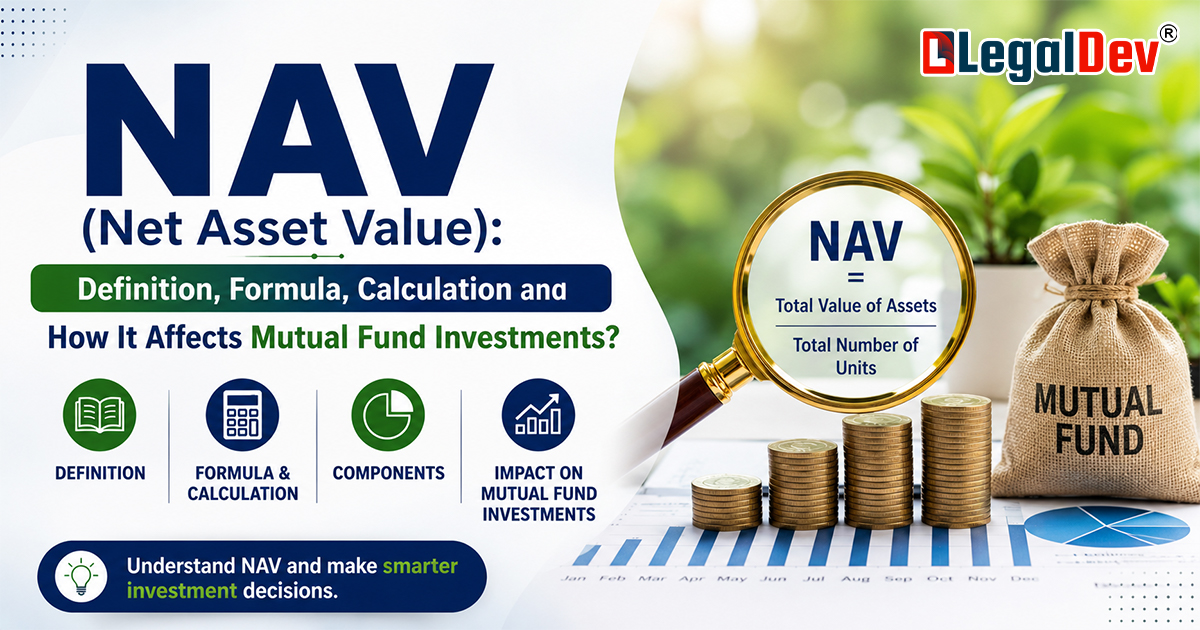

The phrase NAV in Mutual Funds refers to the Net Asset Value, which measures the net worth of an investment scheme per unit. It serves as an official accounting scorecard, reflecting the cumulative valuation of all financial holdings within a portfolio on a per-unit basis. For an active investor, this specific figure dictates the exact transaction price you pay to purchase fresh fund units or receive when you sell your holdings back to the asset management company.

[MUTUAL FUND UNIT SCORECARD]

└── Total Portfolio Securities & Cash Assets

└── LESS: Operational Fees & Administrative Liabilities

└── EQUALS: Total Net Asset Value

└── DIVIDED BY: Outstanding Investor Units = Daily NAV

Think of this metric as a daily tracking report generated by the fund house. Most newly launched portfolios debut with an initial price of ₹10 during their promotional New Fund Offer stage. As the underlying assets gain value over multiple years, this baseline price increases naturally. Here's what most people get wrong: investors often assume a low baseline price makes a fund a cheap bargain, or that a high value indicates an overpriced option. The baseline figure simply represents a mathematical calculation of current portfolio size divided by unit volume, rather than a signal of future performance or intrinsic value.

How Is NAV Calculated for Mutual Funds?

The domestic fund industry operates under standardized rules that govern how an Asset Management Company handles daily asset valuations. Once the public trading floors close for the day, the managers tally the absolute current value of all stocks, bonds, corporate debts, and liquid cash balances. They then subtract accumulated operational debts and management expenses from this total before dividing the final amount by the total outstanding units.

Standardized Calculation Steps

The internal accounting system follows a strict multi-step process to generate the daily valuation:

-

Asset Tallying: The system compiles the complete market value of all underlying securities, liquid bank cash, and pending dividend payments.

-

Liability Deduction: Managers subtract all internal fund expenses, administrative fees, and accrued management costs.

-

Unit Division: The remaining net asset pool is divided by the total number of outstanding units held by investors.

Mathematical Equation

To find this value mathematically, use the standard industry formula:

Total Assets − Total Liabilities

NAV = ------------------------------------------------

Total Number of Outstanding Units

Real-World Mathematical Examples

Let's look at an explicit scenario to see how this accounting math works out in practice. Imagine a specific portfolio that possesses gross securities and cash reserves totaling ₹5,000 crores. At the same time, the managing institution accumulates operational debts and accrued fees amounting to ₹50 crores. If the total number of outstanding units distributed among the public sits at 100 crores, the calculation is structured as follows:

₹5,000 Crores − ₹50 Crores ₹4,950 Crores

NAV = ───────────────────── = ─────────────── = ₹49.5 per Unit

100 Crores Units 100 Crores Units

To understand how units are credited to your personal account based on these figures, consider a simpler individual transaction. If you choose to invest a fixed sum of ₹5,000 into a specific portfolio that features a current unit rate of ₹500, your ledger will be credited with exactly 10 individual units ($\text {₹5,000} \div \text {₹500} $).

To see why a low unit price does not give you an automatic financial advantage, look at a scenario where you split a sum of ₹1 lakh between two different funds:

-

Portfolio Alpha: Features a current asset price of ₹10. Your capital split gives you exactly 10,000 units ($\text {₹1,00,000} \div \text {₹10} $).

-

Portfolio Beta: Features a current asset price of ₹20. Your capital split gives you exactly 5,000 units ($\text {₹1,00,000} \div \text {₹20} $).

The underlying assets for both pools include diverse selections of equities, bonds, and cash reserves, while your liabilities cover ongoing fund management costs. The final number simply provides a clear snapshot of current value, which is updated at the close of every active trading session.

How is NAV Relevant to Investors?

The per-unit value is highly relevant because it dictates the official price tag for your purchase and redemption transactions. However, building an entire long-term plan around this single metric can skew your results. Choosing a portfolio simply because its per-unit value looks cheap is identical to buying a random penny stock without evaluating the underlying organization's balance sheet.

The per-unit value merely tells you what a single share of that fund is worth today. Your final decisions should depend entirely on your long-term wealth targets, personal risk comfort zone, and intended investment timeline. Chasing a specific number on a daily pricing sheet should never take priority over checking the historical capability of the management team.

What is the Difference Between NAV & Market Price?

A common point of confusion for casual savers is mixing up a fund's daily value with a standard stock's market price. These two metrics operate under completely different structural frameworks.

[PRICING AVAILABILITY MATRIX]

└── Listed Equities ──────► Updates Continually ──► Trading Live via Exchange Order Book

└── Mutual Fund Units ────► Calculates Once ──────► Post-Market Closing Price Evaluation

A stock's price moves constantly throughout the day based on live buy and sell orders on public exchanges. For NAV in Mutual Funds, the asset management company calculates the valuation exactly once per day after the markets close. This daily calculation uses the official closing prices of all securities held in the portfolio.

While shares of individual companies trade live based on supply, demand, and media attention, mutual fund units are processed differently. You buy or sell fund units directly through the asset management company at the fixed daily value, bypassing the intraday price swings seen on stock exchanges. This structural setup is why mutual fund pricing feels much more steady compared to the fast-paced movements of individual stocks.

How Does Investment Timing Affect NAV?

The specific time you submit your transaction determines the exact pricing rate applied to your account. Under guidelines established by the Securities and Exchange Board of India (SEBI), your money must clear specifically bank criteria to secure a desired rate.

Standard Portfolio Processing Windows

For the majority of equity and debt schemes, the transaction processing windows operate under the following rules:

-

Purchase Windows: You secure the current day's pricing rate if your capital successfully reaches the asset management company's bank account before the 3 PM deadline.

-

Redemption Windows: If you submit a formal sell request before 3 PM, your transaction settles at that day's closing rate. Submitting your request after 3 PM bumps your settlement price to the next business day's closing rate.

Specialized Low-Duration Products

Liquid and overnight schemes use tighter operational cut-offs to manage short-term capital movements securely:

-

Purchase Cut-off: Applications and cleared funds must be processed by 1:30 PM to secure that day's rate.

-

Redemption Cut-off: The daily processing window closes at 3 PM for departures.

To see this in practice, imagine initiating a transaction of ₹75,000 on March 18, 2025. If the banking network completes the transfer before 3 PM, you secure the closing rate for March 18. If the system logs the clearance at 3:01 PM, your purchase is automatically moved to the closing rate for March 19. Sudden market shifts between those days can change your initial entry point.

Role of NAV in Fund Performance

Many individuals treat a fund's unit value exactly like a corporate stock price, believing a lower number provides a more affordable entry point with higher growth potential. This is a common misconception. The standalone unit value never predicts future performance; it simply reflects the historical path and current size of the fund's asset pool.

A scheme with a per-unit value of ₹200 may indicate years of steady compound growth, while a fund sitting at ₹20 might be completely stagnant. The standalone number tells you nothing about where the value is headed next.

Consider a historical comparison of two separate portfolios from past cycles, where one registered a unit value of ₹215 and the other sat at ₹38. Even though their individual unit values were far apart, their net percentage returns over a multi-year period matched each other closely. The key takeaway here is that while daily price adjustments reflect asset movements, you must evaluate historical returns, operational expense ratios, and your personal timeline to identify a truly successful investment.

Conclusion

The daily net asset value of mutual funds gives people a clear view of what one unit of that mutual fund is worth at any point in time; however, it does not predict how a mutual fund will perform in the marketplace in the future. The level of value assigned to a mutual fund’s unit is not an indicator of that mutual fund’s future potential; it simply reflects where that unit has been in the past and how many times that particular unit has split (been provided with more units). To build an effective portfolio, you need to use factors besides the net asset value, such as your investment goals, risk tolerance and operational cost of funds, to produce a well-diversified portfolio that will assist you with producing long-term wealth.

Frequently Asked Questions

Q1: Why does a low NAV in Mutual Funds not indicate a cheaper or better deal for buyers?

A low unit value simply means the portfolio is either recently launched or has a large volume of outstanding units distributed among investors. It does not mean the fund is underpriced. Your total wealth grows based on the percentage change of the underlying assets, regardless of whether you hold many inexpensive units or fewer high-priced ones.

Q2: How often do fund houses update the per-unit value for standard portfolios?

The asset management company calculates and updates the value exactly once per day after the financial markets close. This calculation is based on the final closing prices of all the stocks and bonds held in the portfolio, ensuring a steady price for all daily transactions.

Q3: What happens to my purchase price if my transaction clears after the 3 PM cutoff?

If your money reaches the fund house's account after the 3 PM deadline, your transaction will be processed using the next business day's closing value. This delay means short-term market shifts between those days could alter your initial investment entry point.

Q4: Do stock prices and mutual fund unit values respond to market forces in the same way?

No, they do not. Stock prices move continuously throughout the day based on live trading activity, supply, and demand on public exchanges. Mutual fund units are not traded live; instead, they are bought or sold at a single fixed price calculated at the end of each day by the fund house.

Q5: Can I use the current unit value of a scheme to predict its future returns?

No, you cannot. The unit value simply provides a snapshot of the fund's current net worth per unit based on its past journey. It holds no predictive power for future performance, which is why smart investors look at historical returns, portfolio costs, and management consistency instead.