.jpg)

To ensure that your daughter achieves her financial goals when she is ready to start life on her own, you will need to implement both short-term and long-term financial planning. If you are concerned about the continuing rise in the cost of living (including education costs) and want to provide for events like her wedding or post-secondary education; and be able to keep your money safe while providing a high rate of investment return; the Sukanya Samriddhi Yojana is the way to go! This Prime Minister backed government scheme provides one of the best investments available today to be used by girls under 10. With an outstanding interest rate (for 2018) of 8.2%, the Scheme allows any legal guardian to begin investing in a girl's future today with as little as Rs. 250 per year and up to Rs. 1.5 lakh per year. Long-term investments (14-20 years) are established through this Scheme to provide significant financial security to your daughter as she pursues her life dreams. We will examine this investment vehicle in greater detail by discussing the structure of the Programme, functional mechanisms, rules through which the Programme operates, and eligibility criteria of the Programme for fiscal year 2026-27.

Sukanya Samriddhi Yojana Interest Rate FY 2026-27

During the first quarter of the financial year 2026-27, which runs from April to June, the scheme’s interest rate was set at 8.2 per cent per annum. The interest is compounded annually, and thereby maximizes how quickly the invested capital grows exponentially over its period.

Compared to current commercial lending or investment options available in the marketplace, this yield is much higher. For many conservative investors, the combination of producing a competitive yield and being 100% safe due to the Government of India backing this scheme makes it an attractive investment option.

To enhance your returns from this scheme, it is important to become familiar with the rules of the internal ledger; specifically, interest earned by the authority is only based on the lowest balance during the period from the fifth through the end of each calendar month. At the end of the financial year, the accumulated interest will be credited to the investor's main balance sheet.

Historical Interest Rates for the Sukanya Samriddhi Yojana

The ministry regularly reviews the interest rates for this scheme. By researching how rates have performed historically, you can identify trends that indicate when this scheme continues to outpace its competition.

|

Year

|

Apr-Jun (Q1)

|

Jul-Sep (Q2)

|

Oct-Dec (Q3)

|

Jan-Mar (Q4)

|

|

2026-27

|

8.2%

|

NA

|

NA

|

NA

|

|

2025-26

|

8.2%

|

8.2%

|

8.2%

|

8.2%

|

|

2024-25

|

8.2%

|

8.2%

|

8.2%

|

8.2%

|

|

2023-24

|

8.0%

|

8.0%

|

8.0%

|

8.2%

|

|

2022-23

|

7.6%

|

7.6%

|

7.6%

|

7.6%

|

|

2021-22

|

7.6%

|

7.6%

|

7.6%

|

7.6%

|

|

2020-21

|

7.6%

|

7.6%

|

7.6%

|

7.6%

|

|

2019-20

|

8.5%

|

8.4%

|

8.4%

|

8.4%

|

|

2018-19

|

8.1%

|

8.1%

|

8.5%

|

8.5%

|

|

2017-18

|

8.4%

|

8.3%

|

8.3%

|

8.1%

|

Interest Rate Comparison: SSY vs FD vs PPF

Placing alternative instruments side by side highlights why this girl-centric path is heavily favored. It offers premium rates while bypassing the market volatility that keeps conservative savers awake at night.

|

Scheme

|

Interest Rate (p.a.)

|

|

Sukanya Samriddhi Yojana (SSY)

|

8.2%

|

|

Bank Fixed Deposits (FD)

|

6% - 8%

|

|

Public Provident Fund (PPF)

|

7.1%

|

SSY Key Highlights & Structural Framework

The layout of this product caters directly to long-term household targets. The core design parameters are arranged cleanly below to provide a structural summary of how the account functions.

|

Particulars

|

Details

|

|

Interest Rate

|

8.2% p.a. compounded annually

|

|

Deposit Period

|

15 years from account opening

|

|

Maturity Period

|

21 years from account opening

|

|

Minimum Investment

|

Rs. 250 per year

|

|

Maximum Investment

|

Rs. 1.5 lakhs per year

|

|

Who Can Open

|

Parents or legal guardians of a girl child below 10 years

|

|

Maximum Accounts Allowed

|

Maximum 2 girl children per family (exceptions for twins/triplets)

|

|

Risk Level

|

Government-backed and highly secure

|

|

Best For

|

Long-term savings for girl child education and marriage

|

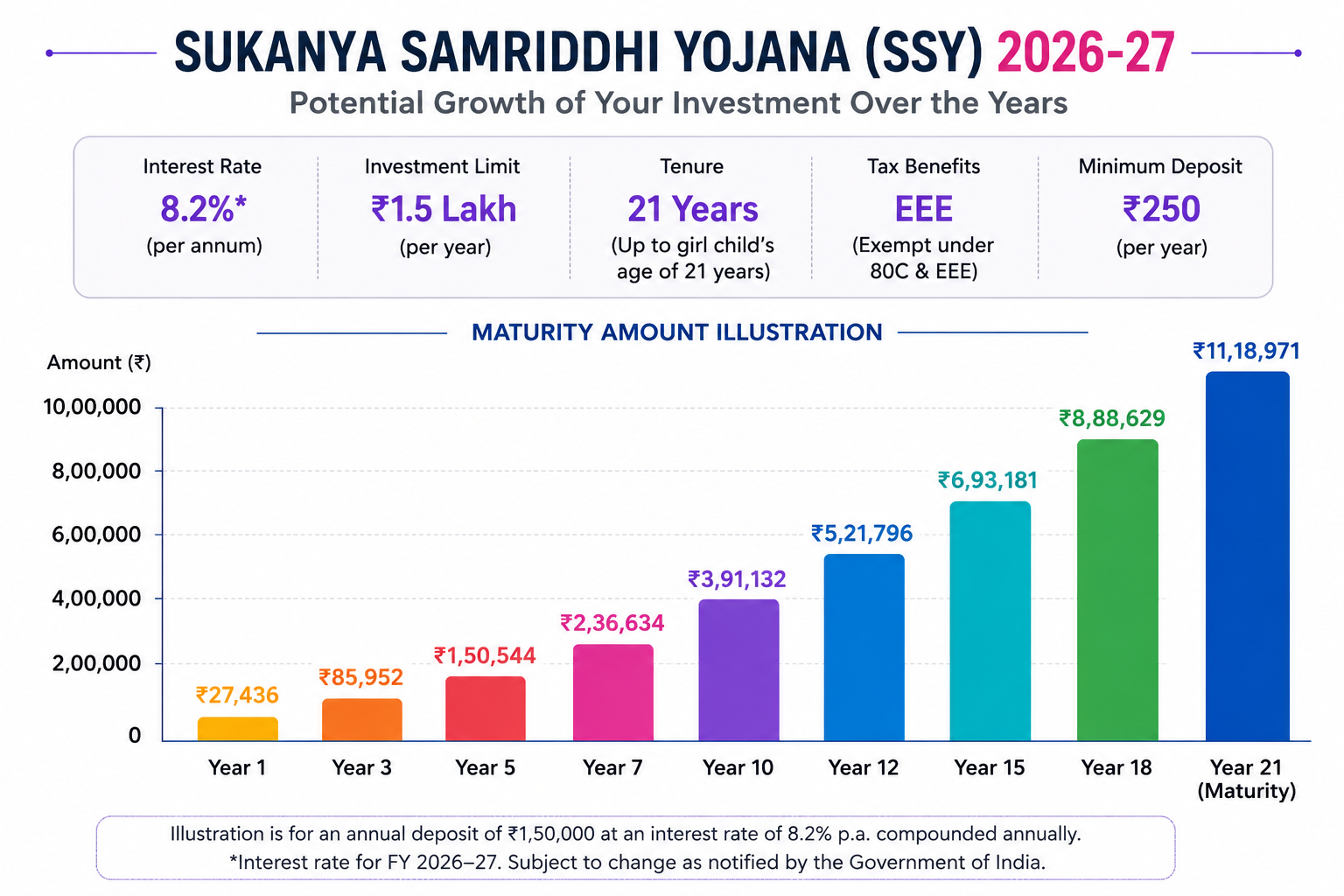

SSY Maturity Amount — Worked Examples

The results are astounding when you leave the capital untouched over 20 years with compounding. You will see that even after your 15-year maximum investment period is up, if you have not withdrawn any funds, you will continue to earn interest on the amount you have accumulated for another 6 years, until the full term expires. This table tells you how much you would have at the end of the term based on different amounts paid on an annual basis using an 8.2% return, not compounded:

• If you paid ₹250 annually, your total capital invested would be ₹3,750. It would mature at ₹11,970.

• If you paid ₹12,500 annually, your total capital invested would be ₹1,87,500. It would mature at ₹5,98,510.

• If you paid ₹50,000 annually, your total capital invested would be ₹7,50,000. It would mature at ₹23,94,040.

• If you paid ₹1 lakh annually, your total capital invested would be ₹15,00,000. It would mature at ₹47,88,079.

• If you paid ₹1.5 lakh annually, your total capital invested would be ₹22,50,000. It would mature at ₹71,82,119.

The bottom line is that if you maximum the contribution amount to ₹1.5 lakhs, then you can take your investment of ₹22.5 lakhs, and at maturity you will have a projected corpus amount of ₹71 lakhs. The velocity of yearly compounding is staggering and provides substantial protection for your daughter's future education from rising educational costs.

SSY Eligibility & Account Opening Rules

If you're aware of what the baseline eligibility requirements are, you'll see that obtaining the correct entry documentation is very simple. This framework means that a parent or legal guardian can establish this account for a resident girl child, as long as she is not older than 10 years of age on the date of entry. There are strict limits on how many families can have accounts under this programme, and a household is limited to a maximum of two such accounts.

There are exceptions to this rule: there can be three such accounts for a guardian who has had two or more births simultaneously, or one birth followed by a twin of the same child, if proof is provided by an actual medical record. Note: legally adopted daughters also have equal rights under this provision if the necessary legal adoption decree(s) is produced. Non-resident Indians are not allowed to open accounts/establish accounts under this arrangement, or if a current account holder moves to NRI status, then they must notify the bank/returns office so that the account may be closed permanently.

SSY Deposit & Operational Rules

To keep your account active and in good standing, it is necessary that you keep yourself aware of the timing of the operations taking place on your account. While your account has an average operational period of twenty-one years, you commit to paying towards your account for fifteen of those years. If you do not deposit the required base amount into your account during that fifteen-year period, your account will be considered in default status. In the event that this occurs, your account can be reactivated by paying the amount of the missing contributions and a penalty of Rs. 50 for each year the account has been in default.

• Minimum Contribution: Rs. 250 must be paid each fiscal year.

• Maximum Limit: The maximum amount you may deposit in any fiscal year is Rs. 1.5 Lakh.

• Maturity Limit: The maximum duration of your account is twenty-one years from the date the account was opened.

• Transaction Channels: Funds can be deposited in your account by cash, cheque, demand draft and by electronic transfer (e.g., ACH).

• Operational Control: The guardian appointed to manage your account will be responsible for monitoring all account transactions until you reach age 18.

SSY Withdrawal & Premature Closure Rules

The existing regulatory framework provides well-defined options for early closure or access to an existing special children’s savings account, should there be a valid reason related to the child’s life events (such as attending college, getting married).

1)How to Close an SSY Account Prematurely

SSY accounts may be closed earlier than 21 years under specific situations:

-

Marrying the Girl Child: Once a girl child reaches age 18, she may apply to close her account. The application must be processed at least one month before her wedding or within three months after the date of marriage (accompanied with valid proof of age).

-

Death of Account Holder: In the unfortunate event of the minor’s death, the full amount in the account will be distributed to the guardian upon submission of the original death certificate.

-

Medical Emergency or Guardian is Deceased: If the account-holder child is diagnosed with a terminal illness or the guardian of the account-holder child has died and the account-holder child is unable to continue to maintain the account due to loss of income, an exception can be requested for consideration.

-

Basis of General Early Closure: If an account is closed for another reason not listed above, the account will earn interest at the lower rate of a post office savings account as opposed to a higher rate of 8.2%.

2. Pre-Maturity Withdrawal Rules

• Limit on Capital Available for Withdrawal: Total withdrawal is limited to no more than 50% of your balance as of the end of the last fiscal year (your account has been in existence).

• Approved Purpose of Withdrawal of Funds: Funds will only be approved for educational tuition purposes, or for paying for wedding management services.

• Age and Minimum Qualification for Qualifying for Withdrawal: Beneficiary must either meet the age requirement of being 18 years old; OR have completed the 10th standard of education.

• Options for Receiving Money: You may either receive one payment cash-in-hand (lump sum) OR five equal payments (annually) over a 5-year period.

• Required Supporting Documents: Provide a Form-3 from your guardian, providing cost itemization (i.e. admission receipt, slip showing has paid for education, a current passbook). The value being requested cannot exceed the actual fee charge by the institution.

Need help with GST? Let our experts handle it for you.

✔ Fast Process ✔ 100% Online ✔ Trusted by Businesses

Sukanya Samriddhi Yojana Tax Benefits

This scheme is highly valued by tax planners because it carries the coveted Exempt-Exempt-Exempt (EEE) status. This status offers tax advantages at every stage of the investment process.

[Stage 1: Investment] ───► Eligible for Section 80C Deduction (Up to Rs. 1.5 Lakh)

[Stage 2: Accumulation] ───► Annual Interest Earned is 100% Tax-Free (Section 10)

[Stage 3: Maturity] ─────► Final Lumpsum Payout is Completely Exempt from Tax

-

Deduction on Deposits: Every rupee contributed on a monthly or annual basis qualifies for a Section 80C deduction, capping out at Rs. 1.5 lakh per year.

-

Tax-Free Interest: The annual interest additions remain fully immune to taxation under Section 10 of the Income Tax Act.

-

Tax-Free Maturity: When the final payout lands after 21 years, both the core principal and the giant pile of interest are distributed without any tax deductions.

Investment Alternative Comparisons

Understanding where to place your savings requires looking at all available paths. This section breaks down how this scheme matches up against other traditional and market-linked avenues.

Comparison of SSY, PPF, NSC, and Mutual Funds

|

Basis

|

Sukanya Samriddhi Yojana (SSY)

|

Public Provident Fund (PPF)

|

National Savings Certificate (NSC)

|

Mutual Funds (Equity)

|

|

Expected Return

|

8.2% p.a.

|

7.1% p.a.

|

7.7% p.a.

|

Market-linked (10%–15% expected long-term)

|

|

Tenure

|

21 years

|

15 years

|

5 years

|

No fixed tenure

|

|

Tax Benefit

|

EEE benefit under Section 80C

|

EEE benefit under Section 80C

|

Section 80C deduction available

|

ELSS funds eligible under Section 80C

|

|

Liquidity

|

Partial withdrawal allowed after 18 years

|

Partial withdrawal after specified years

|

Limited liquidity before maturity

|

High liquidity (except lock-in for ELSS)

|

|

Risk Level

|

Very Low

|

Very Low

|

Very Low

|

Moderate to High

|

|

Best For

|

Girl child education and marriage planning

|

Long-term retirement and tax savings

|

Guaranteed tax-saving investment

|

Long-term wealth creation and inflation-beating returns

|

SSY vs ELSS — Which is Better for Education Planning?

Choosing between guaranteed government returns and equity growth is a common dilemma for families. Here is a direct comparison of their structural features:

|

Basis

|

Sukanya Samriddhi Yojana (SSY)

|

ELSS Mutual Funds

|

|

Returns

|

8.2% p.a. (government-fixed)

|

Market-linked (historically 12%–15%)

|

|

Risk Level

|

Very Low

|

Moderate to High

|

|

Lock-in Period

|

21 years

|

3 years

|

|

Tax Benefit

|

Section 80C + tax-free maturity

|

Section 80C deduction available

|

|

Tax on Returns

|

Fully tax-free

|

LTCG tax applicable above exemption limit

|

|

Liquidity

|

Partial withdrawal after age 18

|

Redemption allowed after 3 years

|

|

Capital Safety

|

Government-backed

|

Subject to market fluctuations

|

|

Best For

|

Guaranteed education or marriage corpus

|

Long-term wealth creation

|

|

Ideal Investor

|

Conservative parents

|

Parents comfortable with equity risk

|

When SSY Makes More Sense

This path is ideal if you want an absolute guarantee on your child's future education fund without exposure to stock market corrections. It guarantees tax-free payouts at maturity, making it a reliable choice for families focused entirely on long-term capital preservation for their daughters.

When ELSS May Be Better

Equity-linked options are well-suited for families with an extended planning window and a healthy appetite for market volatility. If you want to outperform retail inflation over a decade and prefer structural liquidity right after a brief three-year lock-in, equities can help build a larger corpus. This is the part nobody talks about: mixing a secure baseline with a growth engine often delivers the most balanced financial outcome.

Account Opening Documentation & Process

Setting up your account is a straightforward process once you compile the necessary physical forms and identity verifications.

Documents Required for Sukanya Samriddhi Yojana

You will need to present physical copies of these items at your local banking center or post office desk:

-

The official birth certificate of the girl child beneficiary.

-

Verified identity credentials and address proofs belonging to the operating guardian.

-

A certified medical verification sheet if you are opening accounts for multiple births from a single pregnancy order.

-

Standard KYC papers, including your Aadhaar card and Voter ID records.

-

Any supplementary verification files demanded by the branch managers.

Step-by-Step Account Setup Process

To complete your application at a post office branch or a designated bank counter, follow these functional steps:

1.Select Your Branch

Visit the local post office or a participating bank branch where you intend to maintain the investment.

2.Submit Documentation

Fill out the primary application form (Form-1) with clear personal information and attach your physical verification papers.

3.Complete Initial Deposit

Provide your initial account deposit via cash, a signed cheque, or a demand draft, keeping the amount between Rs. 250 and Rs. 1.5 lakh.

4.Processing and Verification

Wait for the administrative personnel to audit your papers, process the transaction, and create your profile.

5.Passbook Issuance

Collect your freshly generated physical passbook, which records your opening balance and marks the formal launch of your account.

Regulatory Forms Directory

The operational lifecycle of the scheme relies on a series of standardized forms. These are readily available at participating institutions or via institutional download portals.

|

Form No

|

Form Type

|

|

Form 1

|

Application for account opening

|

|

Form 2

|

Pay-in-slip

|

|

Form 3

|

Application for Loan/Withdrawal

|

|

Form 4

|

Pass Book

|

|

Form 5

|

Application for transfer of account

|

|

Form 6

|

Application for extension of account

|

|

Form 7

|

Application for pledging of account

|

|

Form 8

|

Application for premature closure of account

|

|

Form 9

|

Application for closure of account

|

|

Form 10

|

Application for cancellation or variation of nomination in an account

|

|

Form 11

|

Application for settlement of an account of the deceased depositor

|

|

Form 12

|

Letter of authority to open or operate an account on behalf of depositor

|

|

Form 13

|

Affidavit

|

|

Form 14

|

Letter of disclaimer

|

|

Form 15

|

Letter of indemnity

|

Bank Integration Options

If you prefer to avoid the post office queue, you can open an SSY account through a commercial bank. For maximum convenience, consider using an authorized institution where you already hold an active savings account.

Guardians can browse the online portal of any approved bank to print out the official application layout. Once filled, this paperwork can be submitted directly at a local service branch. The full roster of verified banks includes:

-

Axis Bank

-

Bank of Baroda

-

IDBI Bank

-

State Bank of India

-

Indian Overseas Bank

-

Union Bank of India

-

Bank of Maharashtra

-

Indian Bank

-

UCO Bank

-

Bank of India

-

ICICI Bank

-

Punjab National Bank

-

Punjab & Sind Bank

-

Canara Bank

-

Central Bank of India

The step-by-step submission rules and documentation criteria remain identical across all these banking partners.

Sukanya Samriddhi Yojana Online Payment

Managing your regular contributions is much easier when using digital channels. You can use the official smartphone app provided by India Post Payments Bank (IPPB) to schedule your automated transfers. This helps you avoid missing annual deadlines and keeps your account active.

1.Fund the Portal Account

Move the desired investment capital from your personal commercial bank account over to your active IPPB ledger.

2.Locate Department Services

Open your smartphone's IPPB application, navigate directly to the DOP Products / Services section, and select the Sukanya Samriddhi Yojana module.

3.Link Your Accounts

Carefully enter your designated SSY account number along with your unique Customer ID code.

4.Configure Your Investment

Specify your target investment amount and set up your preferred standing instruction interval.

5.Confirmation

Verify the transaction receipt once the system confirms that your automated payment routine is successfully linked.

Transferring Your Account: Post Office to Bank

Moving your active account between different offices or banking platforms can be done free of cost. This flexibility is helpful if your family relocates to a different city or state.

To transfer your account, the managing guardian can follow these steps:

-

Visit the Originating Branch: Head over to the specific post office location that currently manages your ledger. The child does not need to attend this meeting.

-

Request the Transfer: Inform the desk official of your plan to move the account and request the appropriate relocation documents.

-

Submit Transfer Forms: Complete the official account transfer sheet and attach your updated KYC documents. The team will verify your records and close out the local files.

-

Visit the Destination Branch: Take the certified records provided by the post office over to your chosen new banking location.

-

Finalize Setup: Present these verified papers alongside your self-attested identification forms to the branch executive. Once processed, you will receive a fresh passbook to track your future contributions.

Conclusion

The Sukanya Samriddhi Yojana will provide a safe and secure means of saving money that is supported by the Government of India, as well as a highly attractive 8.2% interest rate. If you understand the eligibility requirements, make sure that you can make contributions during the 15-year period, and utilize the EEE tax benefits of Section 80C, you should be able to accumulate a large amount of money when you need it for your daughter's post-secondary education and key milestones in her life. In addition, it is important to keep your account active for those 15 years; therefore, make sure to avoid any simple operational mistakes, such as failing to make the annual Rs. 250 contributions, as this may cause your account to become inactive and stop accumulating money. Lastly, take action now by visiting a branch of an authorized bank or post office to begin building a strong financial foundation for your daughter's future!

Frequently Asked Questions

Q1: How is the monthly interest under Sukanya Samriddhi Yojana calculated?

The interest is calculated based on the lowest balance recorded in the account between the fifth day and the end of each calendar month. This accumulated amount is then officially credited to the account balance at the close of every financial year.

Q2: Can a family open three SSY accounts if they have three daughters?

The general rule caps the account limit at two daughters per family. However, an exception is made if a parent has twins or triplets from a single pregnancy order, provided they present valid medical birth certificates to the branch.

Q3: What happens to the account if the girl child changes her residency status to NRI?

Non-Resident Indians are not permitted to open or operate this account. If the beneficiary moves abroad and changes her residency status, the account must be closed immediately, and the existing balance will be paid out.

Q4: Is there a penalty if I fail to deposit the minimum amount in a financial year?

Yes, failing to deposit the minimum requirement of Rs. 250 transforms the account into a default account. You can regularize it by paying the missed minimum balance along with a penalty fee of Rs. 50 for each year it remained inactive.

Q5: Can I withdraw the entire maturity amount before the 21-year period ends?

Full premature closure is allowed only under specific conditions, such as the marriage of the beneficiary after she turns 18, the untimely demise of the child, or extreme medical emergencies. Other early withdrawals are capped at 50% for educational expenses.

Need help with GST? Let our experts handle it for you.

✔ Fast Process ✔ 100% Online ✔ Trusted by Businesses