Physics Wallah Income Tax Notice 2026 — Here Is What Happened

India's edtech sector has been making headlines for all kinds of reasons lately — and the latest one involves Physics Wallah (PW), one of the country's most recognised online education platforms.

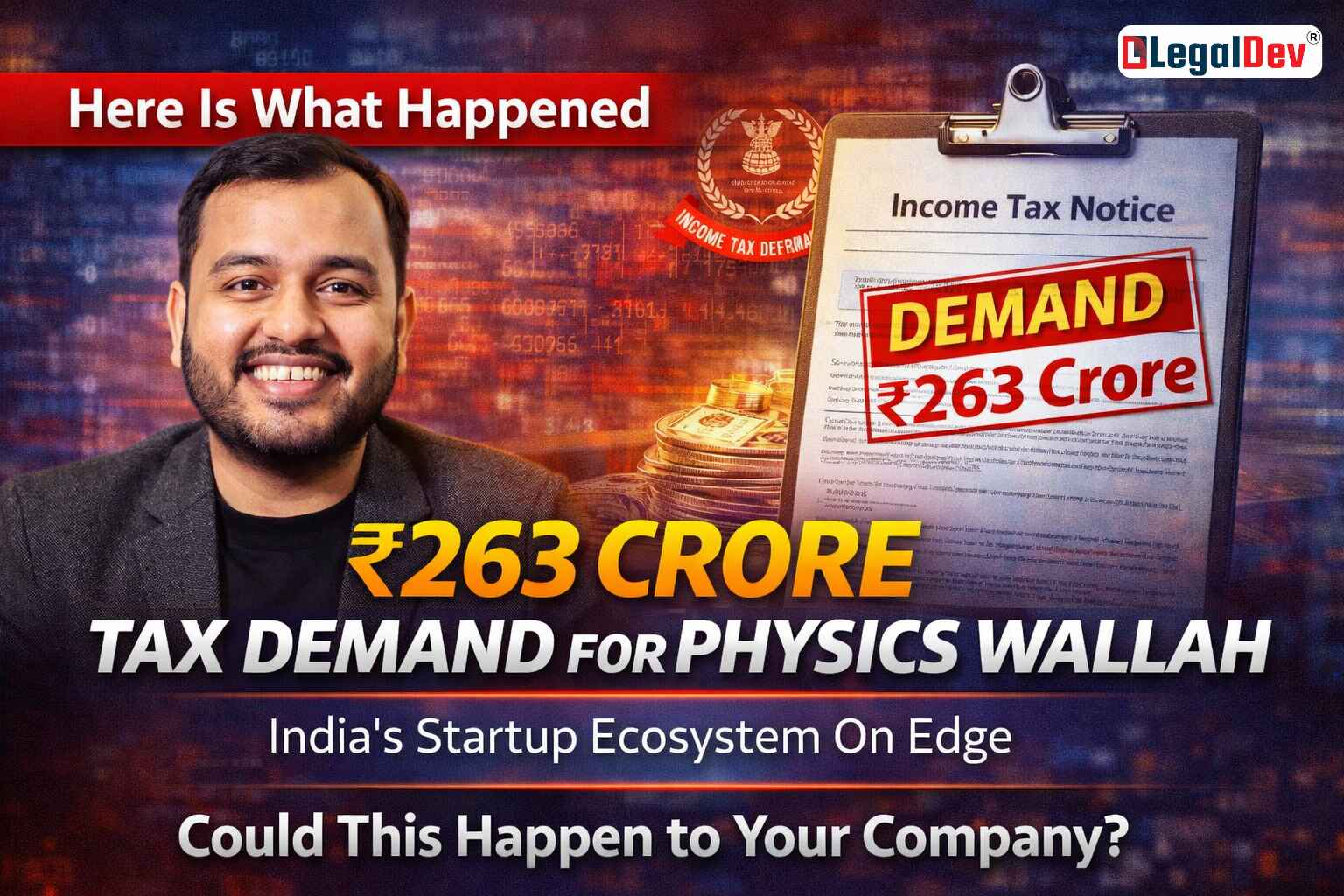

On 16th March 2026, Physics Wallah received an assessment order and demand notice under Section 143(3) of the Income-tax Act, 1961, from the Assessment Unit of the Income Tax Department. The tax demand stands at ₹263.34 crore for Assessment Year 2023-24. The company disclosed this development to stock exchanges on 18th March 2026 and has since stated that it will challenge the order before the appropriate appellate authority.

Now, a ₹263 crore tax notice against a company reporting quarterly revenues of over ₹1,000 crore raises several questions — not just for Physics Wallah , but for every startup, investor, and business owner in India. What went wrong? Could this happen to your company? And what are the practical lessons here?

Let us break this down clearly.

What Is the ₹263 Crore Income Tax Demand Against Physics Wallah

The core issue here is not complicated to understand, even if the tax law behind it is.

During Assessment Year 2023-24, Physics Wallah received investments from various investors, including SEBI-registered Category II Alternative Investment Funds (AIFs). These are funds that pool money from high-net-worth investors and deploy it into companies like Physics Wallah as part of their investment strategy.

The Income Tax Department, in its assessment order, has treated these investments as taxable income rather than as capital received from investors. This reclassification is what led to the ₹263.34 crore demand.

Physics Wallah has made it clear in its regulatory filing that it believes this classification is incorrect and that it has strong legal and factual grounds to challenge the order. The company also clarified that no penalties or compliance irregularities have been identified in the notice — meaning this is an interpretational dispute, not an allegation of wrongdoing.

This distinction matters. The Income Tax Department and the company essentially disagree on how these investment receipts should be treated under the law. That kind of disagreement is not uncommon in startup taxation — and it is exactly the kind of situation where having proper tax structuring and expert legal guidance from day one makes all the difference.

Physics Wallah Financial Performance 2026 — Is the Company in Trouble

Looking at the numbers honestly — no, Physics Wallah is not in financial trouble.

In Q3 FY2026, the company reported revenue of ₹1,082.41 crore — up 33.7% from ₹809.67 crore in the same period last year. Consolidated profit for the same quarter came in at ₹102.27 crore, representing a 33.4% increase from ₹76.72 crore a year earlier.

The user base has also grown meaningfully. Total unique paid users reached 43.7 lakh, up from 36 lakh a year ago. Online paid users grew from 33 lakh to 39.6 lakh, while offline enrolments increased from 3 lakh to 4.1 lakh. That kind of growth across both channels reflects a business that is executing well on its core model.

Physics Wallah 's stock actually rose 7.87% on the day the tax notice was disclosed — a sign that the market is choosing to focus on the company's underlying business performance rather than the tax dispute.

The company has also been making expansion moves. It has approved the incorporation of a new subsidiary — Physics Wallah Student Housing — which will provide hostel and accommodation facilities for students in key cities. Additionally, it plans to invest ₹1.5 crore to acquire a 50% stake in Kay Wellness, broadening its presence beyond core education services.

So while the ₹263 crore demand is significant on paper, for a company operating at this scale with strong cash flows, it is a legal challenge to manage — not an existential threat.

How This Income Tax Case Affects Indian Startups and AIF Investors

This case is genuinely important beyond just Physics Wallah.

India's startup ecosystem has relied heavily on AIF-routed investments over the last several years. Category II AIFs in particular have been a popular vehicle for channelling private equity and venture capital into unlisted companies. If the Income Tax Department's interpretation in this case — that such investment receipts can be treated as taxable income — were to become a broader pattern, it would send serious ripples across the entire startup funding ecosystem.

For investors, it raises the question of how their deployed capital is being classified at the company level. For founders and CFOs, it is a reminder that the structure through which funding is received matters enormously from a tax perspective. Receiving money and paying tax on it as income is a fundamentally different outcome than receiving it as capital — and the difference can amount to crores.

This is also a reminder that income tax notices under Section 143(3) are scrutiny assessments — meaning the department has gone through the company's accounts in detail before raising this demand. Any business that receives significant external funding, whether through AIFs, venture capital, or angel investors, needs to ensure that the tax treatment of those receipts is clearly documented and defensible.

Physics Wallah Consumer Court Order — What Service-Based Businesses Must Know

Alongside the tax notice, a consumer court has directed Physics Wallah to pay ₹50,000 as compensation in a case where deficiency in service was found.

While the amount is small in the context of the company's scale, it is a reminder that service quality obligations apply to edtech platforms just as much as they do to any other business. Students and parents who pay for online education courses have legal recourse if the promised service is not delivered — and consumer courts have been increasingly willing to rule against companies in such cases.

For any edtech business or subscription-based service provider, this is worth paying close attention to.

Key Tax Compliance Lessons Every Indian Business Must Take From This Case

The Physics Wallah income tax situation is not just a news story — it is a practical case study in what can go wrong when tax structuring is not handled carefully from the beginning.

A few key takeaways for business owners, founders, and directors:

Document how every investment receipt is treated. Whether it is from an AIF, a venture capital firm, or an angel investor, the tax treatment of that receipt must be clearly established and consistently applied from day one.

Do not assume that SEBI registration protects you from income tax scrutiny. The fact that funds came from a SEBI-registered AIF did not prevent the Income Tax Department from questioning the treatment of those receipts. Tax law and securities law operate independently.

Scrutiny assessments under Section 143(3) are detailed and serious. If your company receives a notice under this section, respond with the help of a qualified tax professional immediately. The timelines for response are strict and missing them has consequences.

Proactive tax compliance saves far more than it costs. A ₹263 crore tax demand, even if eventually set aside on appeal, involves significant legal costs, management time, and distraction from core business activities. Getting the structuring right from the start is always cheaper.

What Should You Do If Your Business Receives an Income Tax Notice

If your business has received external funding and you are not confident about how those receipts have been treated for income tax purposes, now is a good time to get that reviewed.

Do not ignore the notice. Every income tax notice has a deadline for response and ignoring it leads to ex-parte orders that are far harder to challenge later.

Read the notice carefully. Understand whether it is a scrutiny assessment under Section 143(3), a defective return notice, or a demand for outstanding tax. Each type requires a different response.

Gather all documentation. Investment agreements, board resolutions, valuation reports, and bank statements are all likely to be relevant in a dispute involving funding receipts.

Respond through a qualified tax professional. Income tax proceedings are technical, and the language and content of your response matters significantly to the final outcome.

LegalDev's tax advisory team works with startups, private limited companies, and growing businesses to ensure that their tax positions are sound and defensible — before notices arrive, and after them too. If you have received a notice or want a review of your company's tax exposure, reach out to the LegalDev team for a consultation.

Physics Wallah Tax Notice 2026 — The Bigger Warning for Indian Startups and Founders

Physics Wallah is a strong business with solid fundamentals, and it has the resources and legal standing to contest this tax demand effectively. The company's growth numbers speak for themselves, and its expansion plans suggest a management team that is focused on the long term.

But the broader lesson from this episode is clear — in India's evolving regulatory environment, tax compliance is not something that can be treated as an afterthought. The way funding is received, structured, and reported has direct tax implications, and those implications need expert attention.

Whether you are running a private limited company, managing a funded startup, or scaling a business that takes external investment — understanding your tax exposure is not optional. It is foundational.