The new tax regime under Section 115BAC has changed how millions of Indians think about tax planning — and honestly, for good reason. Relaxed slab rates, a higher standard deduction, and tax-free income up to ₹12 lakh make it genuinely attractive for taxpayers who don't have elaborate investment portfolios or complex deduction structures. It's not just about saving tax — actually, it's about simplifying the whole process entirely. Less documentation, fewer compliance steps, and a cleaner calculation. This article breaks down everything: slab rates, what's allowed, what's not, switching rules, and a worked example showing exactly how much you could save.

What Is Section 115BAC — The New Tax Regime?

Budget 2020 first introduced Section 115BAC as an alternative tax structure offering lower rates with fewer exemptions. Budget 2023 then amended it further — tweaking the slab rates and making the new regime the default option for all taxpayers.

Under this structure, a simpler tax framework replaces the complicated web of investments and deductions that the old regime demanded. Taxpayers pay lower rates without needing to park money in specific instruments, maintain paper trails of donations, or calculate allowance exemptions individually.

And the benefits go beyond just the slab rates. Section 115BAC offers more favourable surcharge rates, a higher rebate, and a standard deduction — all without requiring elaborate tax planning. Less work. Potentially less tax.

Both individuals and HUFs can use it. Residents, non-residents, and senior citizens all qualify. The new regime is the default — but if you want the old regime, you can still opt for it, as long as you do so before the ITR filing deadline. Miss that window and you're locked into the new regime for that year, even if the old one would have saved you more.

Key Highlights of the New Tax Regime at a Glance

Before diving into the details, here are the numbers that matter most:

-

Basic exemption limit: ₹4 lakh

-

Tax rebate available: up to ₹60,000

-

Tax-free income for general taxpayers: up to ₹12 lakh

-

Tax-free income for salaried individuals: up to ₹12.75 lakh (due to standard deduction)

-

Standard deduction for salaried: ₹75,000

-

HUFs: eligible under the new regime

-

Deductions like HRA, 80C, and 80D: not available

Most people focus only on the rebate number. But the combination of relaxed slabs plus standard deduction plus rebate is what actually pushes tax-free income higher for salaried taxpayers specifically.

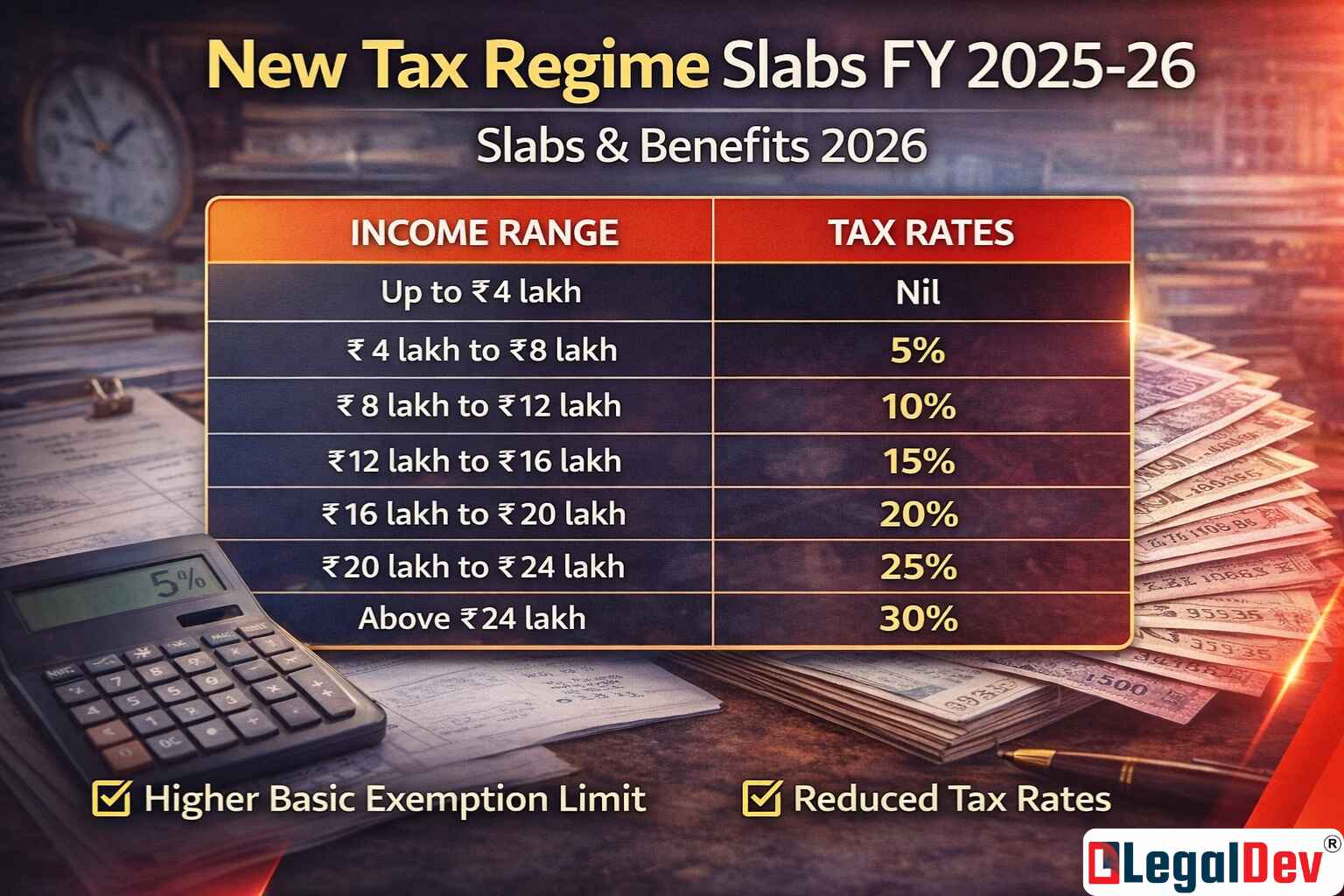

Income Tax Slab Rates Under Section 115BAC for FY 2025-26 (AY 2026-27)

Here's exactly what the new regime tax slabs look like for FY 2025-26:

|

New Tax Slabs FY 2025-26 (AY 2026-27)

|

New Tax Rates

|

|

Up to ₹4 lakh

|

Nil

|

|

₹4 lakh to ₹8 lakh

|

5%

|

|

₹8 lakh to ₹12 lakh

|

10%

|

|

₹12 lakh to ₹16 lakh

|

15%

|

|

₹16 lakh to ₹20 lakh

|

20%

|

|

₹20 lakh to ₹24 lakh

|

25%

|

|

Above ₹24 lakh

|

30%

|

Budget 2026 brought no changes to these slab rates. What you see above is what applies for the current filing season.

The slab structure is progressive — and the jump from 5% to the top rate of 30% happens across a wider band than most people expect. That gradual build is part of what makes the new regime attractive for mid-range income earners.

Rebate Under the New Tax Regime — How Tax-Free Income Works

Resident taxpayers with taxable income below ₹12 lakh pay zero tax under the new regime. That's because of a rebate of up to ₹60,000 available under Section 87A — which effectively wipes out the tax liability for incomes at or below that threshold.

For salaried individuals, the math goes one step further. The ₹75,000 standard deduction reduces gross salary before the slab rates even apply. So a salaried person earning ₹12.75 lakh gross ends up with ₹12 lakh taxable income — and that lands them right within the rebate zone. Zero tax. Nothing to pay.

That's the effective tax-free ceiling for salaried taxpayers: ₹12.75 lakh gross salary. And for non-salaried individuals, the ceiling is ₹12 lakh of taxable income. The distinction matters — and this alone can make a big difference to how you structure your income reporting.

Section 115BAC Deductions and Exemptions That Are Allowed

The new tax regime strips away most deductions — but not all of them. Here's what you can still claim.

Chapter VI-A Deductions

-

Employer's contribution to NPS account under Section 80CCD(2) — up to 14% of salary (increased from 10% in Budget 2024, applicable from FY 2024-25 onwards)

-

Additional employee cost deduction under Section 80JJAA

-

Deduction for amounts deposited in the Agniveer Corpus Fund under Section 80CCH(2)

Salary-Related Allowances

-

Standard deduction of ₹75,000

-

Exemption on voluntary retirement under Section 10(10C)

-

Gratuity exemption under Section 10(10)

-

Leave encashment exemption under Section 10(10AA)

-

Transport allowance for specially-abled employees

-

Conveyance allowance for job-related travel

-

Travel compensation for tours or transfers

-

Daily allowances for duty-related expenses away from the workplace

-

Perquisites for official purposes

House Property

-

Interest on home loan for let-out property under Section 24 — claimable without any upper limit

Other Sources

-

Gifts up to ₹50,000

-

Deduction of ₹25,000 against family pension income

One important forward-looking note: under the new Income Tax Act 2025, the new tax regime provisions shift to Section 202. But that section only becomes relevant from April-July 2027 onwards — it won't affect the current ITR season running April to July 2026.

Old vs New Tax Regime — Deductions Comparison Table for FY 2025-26

|

Deduction / Exemption

|

Old Regime

|

New Regime

|

|

Section 80C (PPF, NSC, ELSS, Life Insurance, etc.)

|

Up to ₹1.5 lakh

|

Not available

|

|

House Rent Allowance (HRA)

|

Available (actuals-based)

|

Not available

|

|

Standard Deduction (salaried)

|

₹50,000

|

₹75,000

|

|

Section 80D (Health Insurance Premium)

|

Available

|

Not available

|

|

Interest on Housing Loan — Self-Occupied (Section 24)

|

Up to ₹2 lakh

|

Not available

|

|

Section 80G (Charitable Donations)

|

Available

|

Not available

|

|

Leave Travel Allowance (LTA)

|

Available

|

Not available

|

|

Section 80E (Education Loan Interest)

|

Available

|

Not available

|

|

Section 80TTA / 80TTB (Savings Interest)

|

Available

|

Not available

|

|

Professional Tax

|

Available

|

Not available

|

|

Entertainment Allowance

|

Available

|

Not available

|

|

Transport Allowance (Specially Abled)

|

Available

|

Available

|

|

Children's Education Allowance

|

Available

|

Not available

|

|

Income from House Property Loss Set-off

|

Allowed

|

Not available

|

|

Additional Depreciation — Section 32(1)(iia)

|

Available

|

Not available

|

House Property and Business Loss Rules Under the New Regime

This is the part that trips up business owners and landlords the most — and honestly, it's often overlooked.

|

Deduction / Loss

|

Old Regime

|

New Regime

|

|

Self-Occupied House Property

|

Interest on loan up to ₹2 lakh deductible; loss can be set off

|

No deduction for interest; no loss set-off

|

|

Let-Out House Property

|

Interest fully deductible; excess loss can be set off or carried forward

|

Deduction limited to taxable rent; no set-off or carry forward of excess loss

|

|

Business Loss / Unabsorbed Depreciation

|

Set-off and carry forward allowed if conditions are met

|

Not allowed if linked to deductions unavailable under the new regime (e.g., Section 35)

|

|

Section 35 Deduction Loss

|

Can be carried forward and set off in future years

|

Cannot be set off if the underlying deduction isn't allowed under the new regime

|

Section 115BAC Deductions and Exemptions That Are NOT Allowed

The list of what's disallowed is long. But knowing it clearly helps you make the right choice between regimes.

Chapter VI-A

-

Section 80TTA and 80TTB

-

Section 80C, 80D, 80E, and most others — except 80CCD(2) and 80JJAA

-

Employee's own contribution to NPS

-

Donations to political parties or trusts

Salary

-

Professional tax and entertainment allowance

-

Leave Travel Allowance (LTA)

-

House Rent Allowance (HRA)

-

Allowances to MPs/MLAs

-

Helper allowance

-

Children's education allowance

-

Other special allowances under Section 10(14)

House Property

-

Interest on housing loan for self-occupied or vacant property under Section 24

Other Sources

-

Minor child income allowance

Business or Profession

-

Additional depreciation under Section 32(1)(iia)

-

Deductions under Section 32AD, 33AB, and 33ABA

-

Scientific research deductions under Section 35(2AA), 35(1)(ii), 35(1)(iia), and 35(1)(iii)

-

Deduction under Section 35AD or 35CCC

-

SEZ unit exemption under Section 10AA

Can You Switch Out of the New Tax Regime?

Yes — but the rules differ depending on whether you're salaried or not.

|

Particulars

|

Salaried Taxpayer

|

Non-Salaried Taxpayer

|

|

Opting out of New Tax Regime

|

Allowed

|

Allowed

|

|

Action required

|

Choose old regime while filing ITR

|

File Form 10-IEA

|

|

Form 10-IEA applicability

|

Not applicable

|

Mandatory

|

|

Form 10-IEA filing frequency

|

Not required

|

Once (valid for future years)

|

|

Switching back to New Regime

|

Allowed anytime

|

Allowed only once in lifetime

|

Salaried taxpayers have it simpler — they just choose at the time of filing. Non-salaried taxpayers with business income must file Form 10-IEA, and once they switch back to the new regime, they can only do that once in their lifetime. That's a one-way door — use it carefully.

Income Tax Calculation Under the New Regime — Worked Example

Let's run through a real number. Mr. Rakesh has a salary income of ₹25 lakh for FY 2025-26 (AY 2026-27).

Taxable income calculation:

|

Particulars

|

Amount

|

|

Income from Salary

|

₹25,00,000

|

|

Less: Standard Deduction

|

-₹75,000

|

|

Taxable Income

|

₹24,25,000

|

Tax liability comparison:

|

Tax Regime

|

Tax Liability

|

|

New Tax Regime

|

₹3,19,800

|

|

Old Tax Regime

|

₹5,69,400

|

By choosing the new tax regime, Mr. Rakesh saves ₹2,49,600 in taxes for the year. That's not a marginal saving — it's nearly ₹2.5 lakh back in his pocket, purely by switching regimes and skipping the old deduction maze.

Final Word — Which Regime Should You Choose?

The new tax regime under Section 115BAC works best for taxpayers with straightforward income and limited deductions — especially those who don't have large home loan interest, HRA claims, or significant 80C investments. The old regime still makes sense if your deductions are substantial enough to pull your effective tax rate below the new regime rates.

Run the numbers both ways before deciding. Use an income tax calculator with your actual deductions to compare the tax liability under both regimes. The regime that produces a lower final tax number is almost always the right call — personal tax planning doesn't need to be more complicated than that.

Frequently Asked Questions

Is Section 80C available under the new tax regime?

No. Section 80C deductions — covering investments in PPF, NSC, ELSS, life insurance premiums, and similar instruments — are not available under the new tax regime. Taxpayers who rely heavily on 80C to bring down their taxable income should calculate whether the old regime ends up being more beneficial despite its higher slab rates.

Is HRA exemption allowed in the new tax regime?

No, HRA exemption is not permitted under Section 115BAC. The new tax regime disallows most salary-based allowance exemptions, including House Rent Allowance. If your HRA claim is significant relative to your salary, that's a factor that could tip the balance in favour of the old regime for you.

Can senior citizens claim relaxed slab rates under the new tax regime?

No. Unlike the old regime, which offered higher basic exemption limits for senior citizens (₹3 lakh) and super senior citizens (₹5 lakh), the new tax regime applies the same slab structure to everyone regardless of age. The basic exemption of ₹4 lakh applies uniformly — which is actually higher than the old regime's threshold for those under 60.

Do I need to file Form 10-IEA to opt for the old tax regime?

Only if you have business or professional income. Salaried taxpayers can simply select the old regime while filing their ITR — no separate form is needed. Non-salaried taxpayers with business income must file Form 10-IEA before the ITR deadline to opt out of the new tax regime for that year.

Has the employer's NPS contribution deduction changed under the new regime?

Yes. From FY 2024-25 onwards, the deduction for employer's contribution to NPS under Section 80CCD(2) was increased from 10% of salary plus DA to 14% of salary plus DA. This increase was announced in Budget 2024 and applies under the new tax regime — making it one of the few deductions that got more generous under Section 115BAC.