Income Tax Surcharge Rate & Marginal Relief for AY 2026-27: Rates, Examples & How It Works

High income — great. But cross certain thresholds, and the government adds a surcharge on top of your regular income tax. That's an additional percentage charged on the tax you already owe, not on your income directly. The good news? If you've just barely crossed one of those thresholds, marginal relief can significantly bring that extra burden down.

Here's a complete breakdown — rates, categories, and real examples — for AY 2026-27.

What Is Income Tax Surcharge?

Surcharge on income tax is an additional levy charged on the income tax payable — not on the income itself. Think of it as a tax on your tax. It applies to taxpayers in higher income brackets and follows the principle of progressive taxation: those earning more, contribute more.

The surcharge is calculated first. Then cess (currently 4%) is applied on the combined total of tax plus surcharge.

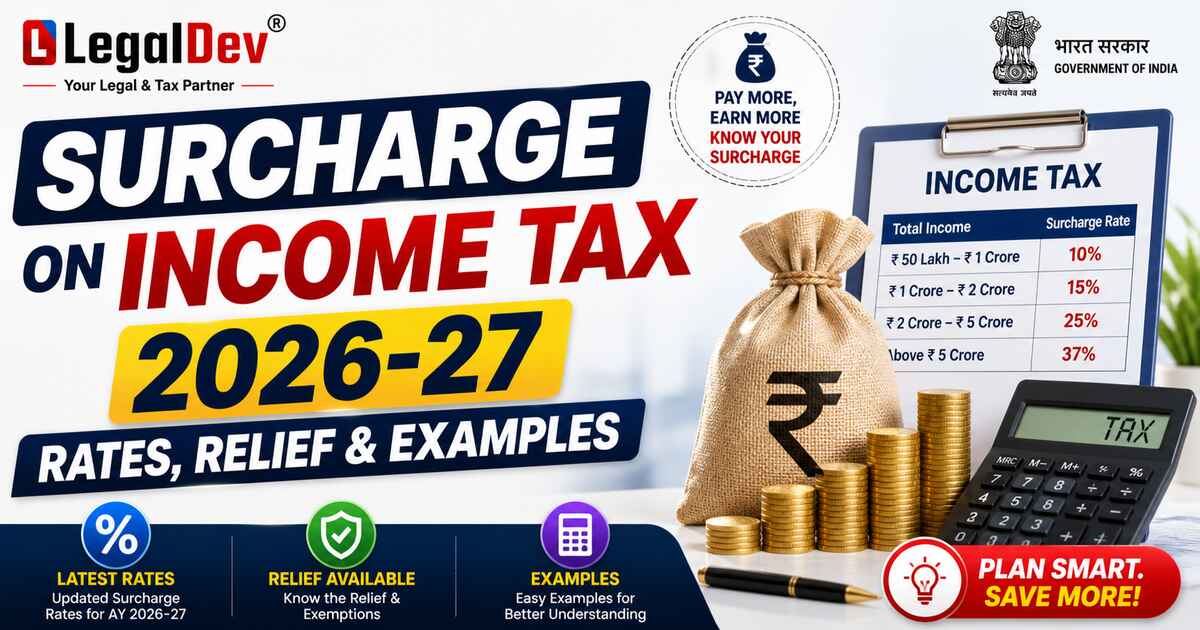

Surcharge Rates for Individuals — Old Regime vs New Regime

For AY 2026-27, the income tax surcharge rate for individuals under both regimes is as follows:

|

Net Taxable Income

|

Surcharge Rate (Old Regime)

|

Surcharge Rate (New Regime)

|

|

Less than ₹50 lakhs

|

Nil

|

Nil

|

|

More than ₹50 lakhs ≤ ₹1 crore

|

10%

|

10%

|

|

More than ₹1 crore ≤ ₹2 crore

|

15%

|

15%

|

|

More than ₹2 crore ≤ ₹5 crore

|

25%

|

25%

|

|

More than ₹5 crore

|

37%

|

25%

|

The key difference between the regimes shows up only at the top. If your income crosses ₹5 crore and you opt for the surcharge new tax regime, the rate is capped at 25% instead of the 37% applicable under the old regime. That's a significant saving at that income level.

Note: For AOPs having only companies as members, surcharge is levied at 15% if total income during the financial year exceeds ₹1 crore.

Surcharge on Capital Gains — The 15% Cap

This one matters for investors. Surcharge on capital gains is capped at 15% — regardless of your total income — for:

-

Dividend income

-

Capital gains under Section 111A (short-term gains on listed equity)

-

Capital gains under Section 112 (long-term gains on unlisted assets)

-

Capital gains under Section 112A (long-term gains on listed equity above ₹1 lakh)

Illustration — Mixed Income with Capital Gains

Mr. A's income for FY 2025-26 looks like this:

-

Business Income: ₹3 crore

-

Capital Gains u/s 112A: ₹50 lakhs

-

Capital Gains u/s 111A: ₹75 lakhs

-

Capital Gains u/s 112: ₹1.25 crore

Total income: ₹5.5 crore. If this were entirely normal income, 37% surcharge would apply across the board.

But here's how it actually works:

-

Capital gains under 111A, 112A, and 112 — surcharge capped at 15%, regardless of the total income level

-

Business income of ₹3 crore — surcharge of 25% applies (income between ₹2 crore and ₹5 crore)

The cap on surcharge on capital gains exists to avoid discouraging investment. It's one of the more taxpayer-friendly provisions in this area.

Surcharge Rates for Domestic Companies

For domestic companies, the income tax surcharge calculation works differently:

|

Net Taxable Income

|

Surcharge (Normal Provisions)

|

Surcharge u/s 115BAA or 115BAB

|

|

Less than ₹1 crore

|

Nil

|

10% (flat)

|

|

More than ₹1 crore ≤ ₹10 crore

|

7%

|

10% (flat)

|

|

More than ₹10 crore

|

12%

|

10% (flat)

|

Companies opting for the concessional tax rate under Section 115BAA or 115BAB pay a flat 10% surcharge — no threshold, no marginal relief applicable in this case.

Surcharge Rates for Foreign Companies

|

Net Taxable Income

|

Surcharge Rate

|

|

More than ₹1 crore ≤ ₹10 crore

|

2%

|

|

More than ₹10 crore

|

5%

|

Surcharge for Firms, LLPs & Local Authorities

Where total income exceeds ₹1 crore, a surcharge of 12% on income tax computed is payable. Marginal relief is available here too — discussed below.

Marginal Relief on Income Tax — What It Is and Why It Exists

Here's the problem marginal relief solves. Suppose you earn ₹51 lakh. Because you've crossed ₹50 lakh, surcharge kicks in — and suddenly your total tax bill jumps by more than what you earned above the threshold. You end up paying ₹1.41 lakh extra in tax for earning just ₹1 lakh more. That's clearly unfair.

Marginal relief limits that excess. Your additional tax liability — due to crossing the threshold — cannot exceed the additional income you actually earned over that threshold.

The formula:

Marginal Relief = (Excess tax payable including surcharge) − (Excess income over the threshold)

Marginal Relief for Individuals — Two Cases Explained

Case 1: Income Between ₹50 Lakhs and ₹1 Crore

Surcharge applicable: 10% on income tax

Example: Individual with total income of ₹51 lakh in FY 2025-26.

-

Tax with 10% surcharge: ₹12,21,000 (before cess)

-

Tax if income were ₹50 lakh: ₹10,80,000 (before cess)

-

Excess tax paid for earning ₹1 lakh more: ₹1,41,000

-

Excess income over threshold: ₹1,00,000

-

Marginal Relief = ₹1,41,000 − ₹1,00,000 = ₹41,000

Final tax liability on ₹51 lakh income: ₹12,27,200 (including cess after marginal relief).

The same surcharge implications apply under the new tax regime — only the income tax slab changes, not the surcharge structure.

Case 2: Income Between ₹1 Crore and ₹2 Crore

Surcharge applicable: 15% on income tax

Example: Individual with total income of ₹1.01 crore in any FY.

-

Tax with 15% surcharge: ₹32,68,875

-

Tax if income were exactly ₹1 crore: ₹30,93,750

-

Excess tax for earning ₹1 lakh more: ₹1,75,125

-

Excess income over ₹1 crore threshold: ₹1,00,000

-

Marginal Relief = ₹1,75,125 − ₹1,00,000 = ₹75,125

Again — the marginal relief income tax calculation protects you from paying disproportionately more just because you crossed a line by a small margin.

Marginal Relief for Firms, LLPs & Local Authorities

Surcharge applicable: 12% where total income exceeds ₹1 crore.

Example: A firm with total income of ₹1.01 crore.

-

Tax with 12% surcharge: ₹32,24,000

-

Tax if income were ₹1 crore: ₹31,20,000

-

Excess tax: ₹1,04,000

-

Excess income over threshold: ₹1,00,000

-

Marginal Relief = ₹1,04,000 − ₹1,00,000 = ₹4,000

Smaller number, but the principle holds. The firm pays only ₹4,000 more than it would have at exactly ₹1 crore — not ₹1,04,000 more.

Marginal Relief for Companies — Two Cases

Case 1: Income Between ₹1 Crore and ₹10 Crore

-

Domestic companies: 7% surcharge

-

Foreign companies: 2% surcharge

Marginal relief applies here. The income tax payable (including surcharge) on income above ₹1 crore cannot exceed the income tax payable on ₹1 crore by more than the amount of income that actually exceeds ₹1 crore.

Case 2: Income Above ₹10 Crore

-

Domestic companies: 12% surcharge

-

Foreign companies: 5% surcharge

Marginal relief again applies. Income tax payable including surcharge on income above ₹10 crore cannot exceed what would have been payable on exactly ₹10 crore by more than the income that exceeds ₹10 crore.

Important: Companies under Section 115BAA or 115BAB pay a flat 10% surcharge with no threshold limit — and therefore no marginal relief is available to them.

A Note on the Income Tax Act 2025

Though the Income Tax Act 2025 takes effect from 1 April 2026, the provisions of the Income Tax Act 1961 continue to apply for AY 2026-27 — since that assessment year covers income earned up to 31 March 2026. So the rates and rules above are based on the 1961 Act, which governs your returns for this year.

FAQs

Q: What is the surcharge rate for individuals with income above ₹5 crore under the new tax regime for AY 2026-27?

A: Under the new tax regime, the surcharge is capped at 25% for individuals with income exceeding ₹5 crore. This is a significant reduction compared to the 37% applicable under the old regime at the same income level. Opting for the new regime at this income bracket can result in considerable tax savings on surcharge alone.

Q: How is marginal relief calculated on income tax for AY 2026-27?

A: Marginal relief is calculated as the difference between the excess tax payable (including surcharge) over the threshold and the excess income earned over that threshold. The formula is: Marginal Relief = Excess tax due to surcharge − Excess income over the slab limit. This ensures your additional tax burden never exceeds your actual additional income.

Q: Is surcharge on capital gains capped at 15% regardless of total income?

A: Yes — surcharge on capital gains under Sections 111A, 112, and 112A is capped at 15%, even if your total income places you in a higher surcharge bracket. This cap applies to dividend income as well. The remaining income (such as business income) is subject to the regular surcharge rate applicable to your total income slab.

Q: Can a firm or LLP claim marginal relief on surcharge?

A: Yes — firms, LLPs, and local authorities are eligible for marginal relief when their total income exceeds ₹1 crore. The surcharge applicable is 12%, and marginal relief ensures that the excess tax paid due to crossing the ₹1 crore threshold doesn't exceed the actual excess income earned over that limit.

Q: Does the 37% surcharge rate still apply under the old tax regime for AY 2026-27?

A: Yes — for individuals with taxable income exceeding ₹5 crore who opt for the old tax regime, a surcharge of 37% continues to apply for AY 2026-27. The 37% rate does not apply under the new tax regime, where the maximum surcharge is 25% even at the highest income levels.

Q: What is the surcharge rate for domestic companies under normal tax provisions?

A: Domestic companies pay a 7% surcharge on income tax when their total income exceeds ₹1 crore but stays within ₹10 crore. For income above ₹10 crore, the surcharge rate increases to 12%. Companies opting for the concessional rate under Section 115BAA or 115BAB pay a flat 10% surcharge regardless of income level, with no marginal relief available.

Q: Is cess calculated on surcharge or only on income tax?

A: Cess is calculated on the total of income tax plus surcharge — not just on the base income tax. So the final tax liability = (Income Tax + Surcharge) + 4% Health and Education Cess on that combined amount. This is why the effective tax rate at higher income levels can be notably higher than the base slab rates suggest.

Q: Does marginal relief apply to companies under Section 115BAA?

A: No — companies that have opted for the special tax rate under Section 115BAA or Section 115BAB are not entitled to marginal relief. Since there is no threshold limit for surcharge applicability under these sections (the flat 10% applies from rupee one of tax), the concept of marginal relief simply doesn't arise.

Q: When does surcharge become applicable for HUFs and AOPs?

A: For HUFs, surcharge becomes applicable when net total income exceeds ₹50 lakh, at the same rates applicable to individuals. For AOPs consisting only of companies as members, surcharge at 15% applies if total income exceeds ₹1 crore during the financial year.

Q: How does the Income Tax Act 2025 affect surcharge rates for AY 2026-27?

A: The Income Tax Act 2025 comes into effect from 1 April 2026, which means it applies from Tax Year 2026-27 onward. For AY 2026-27 — covering income earned up to 31 March 2026 — the Income Tax Act 1961 provisions continue to govern surcharge rates and marginal relief calculations. The 2025 Act does not affect returns filed for the current assessment year.