GST Invoice: Mandatory Fields, Types & Rules You Can't Ignore

Getting your GST invoice wrong isn't just a paperwork problem — it can cost your business the Input Tax Credit it deserves and invite scrutiny you really don't want.

Since GST replaced the old tax regime, every registered business must issue a GST-compliant bill for every sale of goods or services. And it's not just about ticking boxes. Every invoice you raise enters your books of accounts, defines your time of supply, and determines whether your buyer can claim ITC. That's a lot riding on one document.

Here's everything you need to know — what goes on a GST invoice, who issues it, what types exist, and where the e-invoice gst portal fits into all of this.

What Is a GST Invoice?

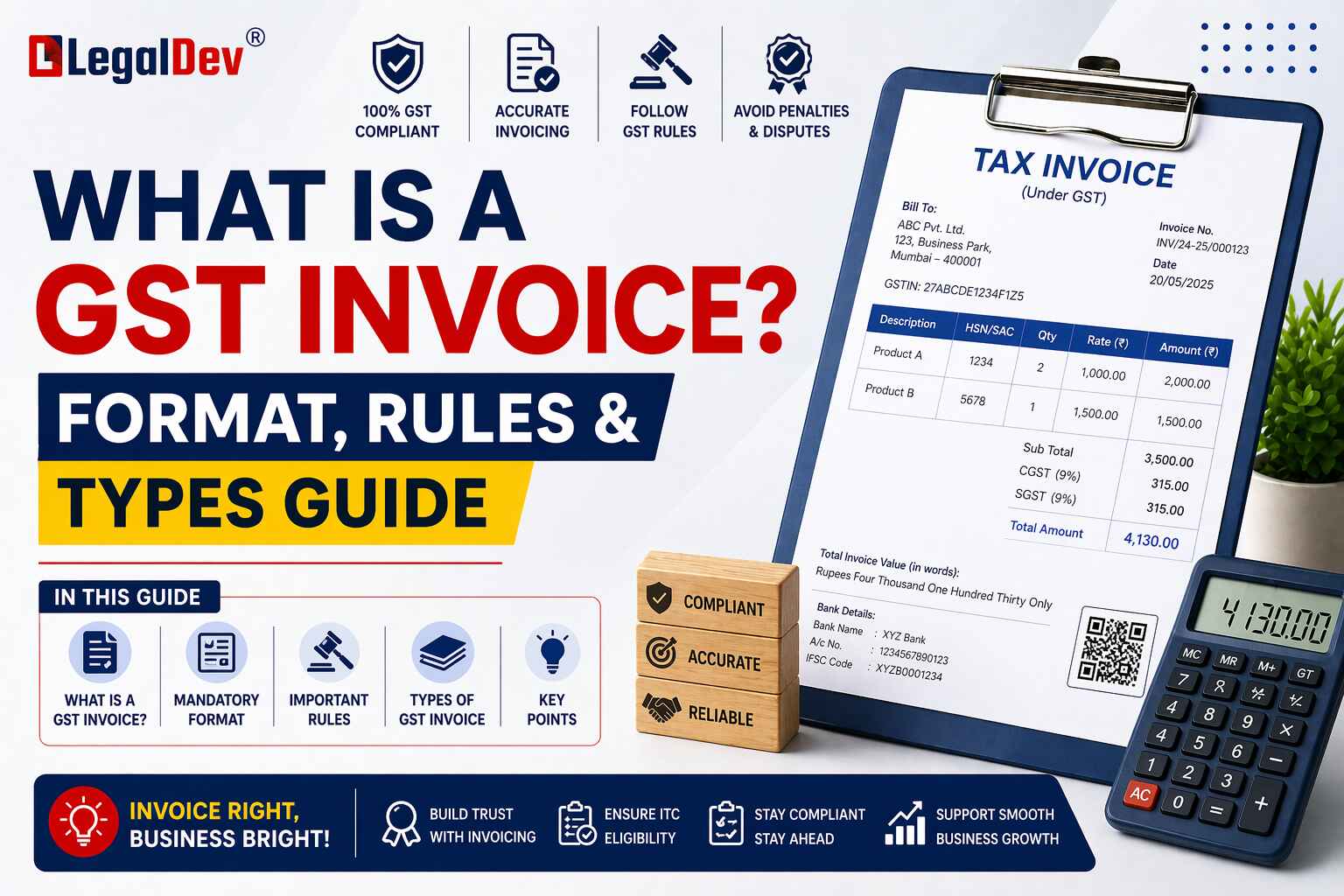

A GST invoice — also called a GST bill — is the official document a GST-registered business issues when selling goods or services. It lists what was supplied, the value, applicable tax rates, and the total amount due.

More than just a receipt, a gst tax invoice acts as legal proof of a transaction. It lets the buyer claim Input Tax Credit and helps both parties stay on the right side of GST compliance. It also records the time of supply, which matters when calculating tax liability.

Under the CGST Rules, the format isn't optional. Every mandatory particular must appear — no exceptions.

Who Needs to Issue a GST Invoice?

Every business registered under the CGST Act — regardless of size — must issue a GST-compliant bill whenever it sells goods or services.

If you're a buyer, you also need a valid gst invoice from your vendors. Without it, you cannot claim Input Tax Credit. Simple as that.

Mandatory Fields on a GST Invoice

A GST invoice must carry specific information. Missing even one field can make it non-compliant. Here's what every original gst bill must include:

-

Invoice number and invoice date

-

Customer name

-

Shipping and billing address

-

GSTIN of both supplier and customer (if the customer is registered)

-

Place of supply

-

HSN code (for goods) or SAC code (for services)

-

Item description, quantity, and unit of measurement

-

Total value

-

Taxable value and any applicable discounts

-

GST rate and tax amount — CGST, SGST, or IGST

-

Whether GST is payable on reverse charge basis

-

Supplier's signature

One thing many businesses miss: if your customer is unregistered and the invoice value exceeds ₹50,000, you must also include the recipient's name, delivery address, state name, and state code. This is non-negotiable under CGST Rules.

GST Invoice Timelines — When Must You Issue It?

The CGST Act doesn't just tell you what to include — it also tells you when to issue the invoice. These deadlines apply to GST tax invoice issuance, revised invoices, debit notes, and credit notes.

For goods: The invoice must be issued before or at the time of removal of goods.

For services: You have 30 days from the date of service delivery to issue the invoice. For banking and financial institutions, the limit extends to 45 days.

Miss these timelines and you may face compliance issues. It's worth setting internal reminders or using invoicing software that handles this automatically.

Types of GST Invoices

Not every transaction calls for a standard tax invoice. Here are the different types you'll encounter:

Bill of Supply

A bill of supply looks similar to a GST invoice but doesn't show any tax amount — because the seller cannot charge GST in certain situations. You issue a bill of supply when:

-

You're selling exempt goods or services

-

You've opted for the Composition Scheme

There's also an invoice-cum-bill of supply — allowed under Notification No. 45/2017 – Central Tax. If you're supplying both taxable and exempt goods to an unregistered buyer, you can club everything into one document instead of issuing two separate ones.

Aggregate Invoice

If multiple invoices in a day are each below ₹200 and all go to unregistered buyers, you can consolidate them into one aggregate invoice. For example — three invoices of ₹80, ₹90, and ₹120 can be merged into a single ₹290 aggregate invoice at day's end. Practical, and completely within the rules.

Reverse Charge Invoice

Under the Reverse Charge Mechanism (RCM), the buyer pays the GST instead of the seller. In this case, the buyer must issue an invoice for the goods or services received and clearly state that tax is being paid under RCM. A separate payment voucher is also required when making the payment to the supplier.

Debit Note and Credit Note

These come into play when an invoice needs to be adjusted after the fact.

A debit note is issued by the seller when the invoice amount was lower than it should have been — either the taxable value or the tax amount was understated.

A credit note is issued when the invoice value needs to come down — if the taxable value or tax was overstated, if the buyer returns goods, or if the services turned out to be deficient.

Can You Revise GST Invoices Issued Before Registration?

Yes. Under GST, all dealers must apply for provisional registration before receiving their permanent GST registration certificate. During this interim period, you may have already issued invoices.

Once your permanent certificate arrives, you have 1 month to issue revised invoices against every invoice raised between the GST implementation date and your registration date. This ensures your earlier transactions are properly documented under the GST framework.

GST Invoicing Under Special Cases

Certain industries get some flexibility on invoice formats. Banking companies, financial institutions, passenger transport providers, and insurers are among those where the government has allowed relaxed formats. The core compliance requirements still apply — just the format has some wiggle room.

How Many Copies of a GST Invoice?

For goods: 3 copies (original for buyer, duplicate for transporter, triplicate for supplier)

For services: 2 copies (original for buyer, duplicate for supplier)

E-Invoicing Under GST — What's Changed?

Since 2020, the GST department has mandated e-invoicing for eligible B2B transactions. Under this system, invoices are authenticated in real-time by the GSTN through the e invoice gst portal before they're shared with the buyer.

Instead of generating the invoice directly, eligible businesses upload invoice data to the gst e invoice portal — currently accessible at einvoice1.gst.gov.in — where it gets an Invoice Reference Number (IRN) and a QR code. That authenticated document is then your official gst e invoice.

E invoicing is currently mandatory for businesses with a turnover above ₹5 crore. The threshold has been progressively reduced since the system launched, and the expectation is that it will eventually cover most registered businesses. If you're using accounting software, most platforms now integrate directly with the gepp e invoice system, making the process fairly seamless.

The gst e invoice portal also enables tax authorities to pre-validate data, which reduces mismatch errors and makes reconciliation far easier during filing.

How Many Copies of Invoice Must Be Issued?

|

Transaction Type

|

Copies Required

|

|

Goods

|

3 (buyer, transporter, supplier)

|

|

Services

|

2 (buyer, supplier)

|

Making Your Invoice GST Compliant — Quick Checklist

Before you send any gst bill, run through this:

-

GSTIN of both parties mentioned (where applicable)

-

HSN/SAC code correct for your supply

-

Invoice number follows a sequential series

-

Place of supply clearly stated

-

Tax breakup — CGST/SGST or IGST — shown correctly

-

RCM applicability mentioned if relevant

-

Digital signature if using DSC

A bill with gst that skips any of these isn't just incomplete — it's non-compliant, and it can block your buyer's ITC claim.

GST Bill Online — Tools and Options

You don't need to build invoices from scratch. Several platforms let you generate a gst bill online — from the official GST portal to accounting tools like billdev, Tally, Zoho Books, and tide invoicing. Most of these are already integrated with the gst e invoice portal for e-invoicing eligible businesses.

For smaller businesses that aren't yet under the e-invoicing mandate, a well-structured Excel template or invoicing tool with a gst bill sample format works just fine — as long as every mandatory field is present.

FAQs

Q: What is the difference between a GST invoice and an e-invoice?

A: A GST invoice is the standard tax document issued by a registered supplier for any sale. An e-invoice is a GST invoice that has been electronically authenticated by the government through the gst e invoice portal, generating an IRN and QR code. E invoicing is mandatory for B2B transactions above certain turnover thresholds.

Q: What details are mandatory on a GST invoice for an unregistered buyer above ₹50,000?

A: For unregistered recipients where the invoice value exceeds ₹50,000, you must include the recipient's name and address, the delivery address, and the state name and code. These details are mandatory under CGST Rules and cannot be skipped.

Q: What is the time limit for issuing a GST tax invoice for services?

A: For services, the GST invoice must be issued within 30 days from the date of supply. For banks and financial institutions, this extends to 45 days. Missing this window can create compliance issues during GST return filing.

Q: What is a self-invoice under GST and when do you need to issue one?

A: A self-invoice is issued by the buyer when purchasing from an unregistered supplier under the Reverse Charge Mechanism. Since the unregistered supplier cannot issue a valid GST bill, the recipient raises the invoice themselves to account for and pay the applicable GST.

Q: Is the invoice serial number mandatory under GST invoicing rules?

A: Yes, maintaining a strict sequential invoice serial number is mandatory under GST. If you need to change the format of your series, you must inform the GST officer in writing and state the reasons. Random or non-sequential numbering is not permitted.

Q: Can I digitally sign a GST invoice using a DSC?

A: Yes. A GST compliant invoice can be digitally signed using a Digital Signature Certificate (DSC). This is especially common for businesses that generate high invoice volumes through accounting software or the gst e invoice portal.

Q: What is the difference between invoice date and due date on a GST bill?

A: The invoice date is when the gst invoice was created and issued. The due date is the payment deadline agreed between the buyer and seller. Both can appear on the same bill with gst, but they serve different purposes — one establishes time of supply, the other governs payment terms.

Q: When should a bill of supply be issued instead of a GST invoice?

A: A bill of supply is issued when the supplier cannot charge GST — either because they're selling exempt goods/services or because they're registered under the Composition Scheme. It looks similar to a goods and service tax invoice but does not show any tax amount.

Q: How does e-invoicing work on the einvoice1gst portal?

A: Businesses upload invoice data to the gst e invoice portal (einvoice1.gst.gov.in). The GSTN authenticates the data and returns an Invoice Reference Number (IRN) along with a digitally signed QR code. This authenticated document becomes the valid gst e invoice that can be shared with the buyer.

Q: What is an aggregate invoice under GST and when can it be used?

A: An aggregate invoice is used when multiple supplies to the same unregistered buyer in a day are each below ₹200. Instead of issuing separate invoices for each transaction, the seller can consolidate them into one aggregate or bulk invoice at the end of the day.