Form 15H: What It Was, Who Could Use It, and What Changed in April 2026

If you're searching for Form 15H in 2026 — you're not alone. But there's something you need to know upfront: the form has been replaced. From 1st April 2026, the old 15 g 15 h form system no longer applies. A new unified declaration, Form 121, has taken its place.

This guide explains what Form 15H was, who it was meant for, and exactly what changed — so you're not filing the wrong thing or missing a step.

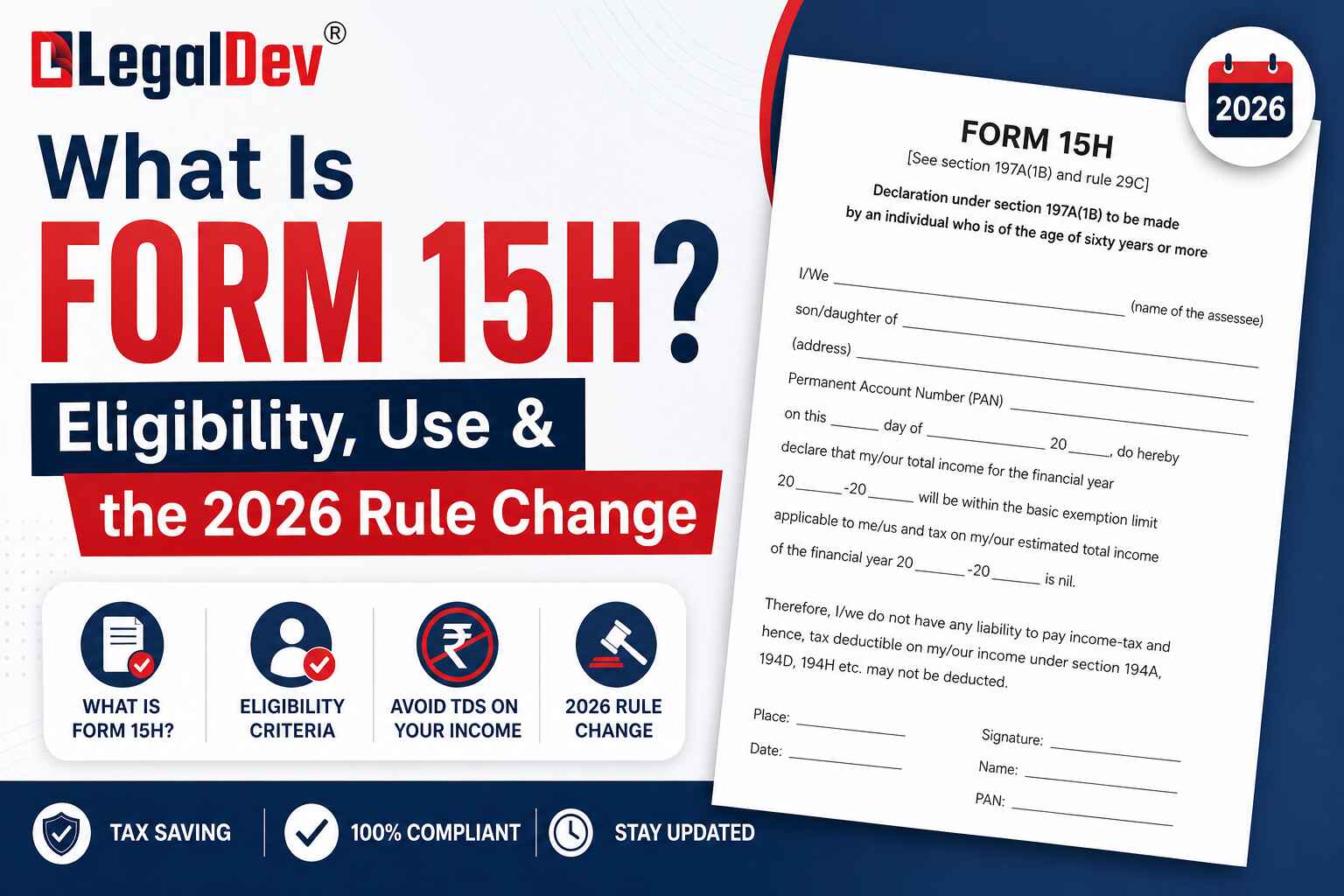

What Is Form 15H?

Form 15H was a self-declaration form for resident senior citizens. By submitting it, a senior citizen could tell the payer — a bank, post office, or mutual fund — not to deduct TDS from their eligible income, provided their total estimated tax liability for the year was nil.

The form didn't make any income tax-exempt by itself. It simply said: "My income won't result in any tax — so please don't deduct tax at source." If the declaration was valid, the payer stopped the TDS deduction.

It was especially useful for fixed deposit interest, recurring deposit interest, dividend income, and similar earnings — the kind of income most retirees depend on.

Who Could Submit Form 15H?

The 15h form was strictly for resident individuals aged 60 years or above. Companies, HUFs, and partnership firms were not eligible — only individual senior citizens.

Two conditions had to be met:

-

Your estimated total income for the financial year must result in nil tax liability

-

A valid PAN card was mandatory — without it, the declaration was considered invalid

If you had multiple accounts or multiple deductors (say, fixed deposits in three different banks), you had to submit the form separately to each one. One submission didn't cover all.

What Was Form 15H Actually Used For?

The main point was simple: senior citizens shouldn't have to pay tax upfront on income they're not ultimately liable for, and then wait months to claim a refund. The 15h form solved that.

It was commonly used for:

-

Bank fixed deposit and recurring deposit interest

-

Post office deposit interest

-

Dividend income

-

EPF withdrawals (via the related 15 g epf form or 15H for those 60+ years)

-

Other specified income payments

For EPF specifically — if a senior citizen was withdrawing from their PF account and their income was below the taxable limit, submitting Form 15H prevented TDS under Section 192A. The 15 g form for pf worked similarly for those under 60.

How the Form Was Submitted

The process was fairly straightforward. The declarant would fill out Form 15H and submit it to the deductor — the bank, post office, mutual fund, or employer — at the beginning of the financial year, or at the time of withdrawal in the case of PF.

Many banks, including SBI, allowed online submission. The 15 g form SBI and 15H could both be submitted through net banking or at the branch. The payer would then not deduct TDS for the remainder of that financial year.

One important point: the form was valid only for one financial year. So if you needed it next year too, you'd submit it again at the start of that year.

What Changed in 2026 — The Form 121 Update

This is the part most people searching in 2026 need to understand clearly.

From 1st April 2026, under the new Income Tax Rules 2026, the old Form 15H (and Form 15G for those below 60) have been replaced by a single unified form — Form 121.

The 15h declaration as you knew it is no longer the active filing form. If you or a family member is submitting a TDS declaration for Tax Year 2026–27 onwards, you need Form 121 — not Form 15H.

The purpose stays the same: declare that your income is below the taxable threshold so TDS doesn't get deducted. The structure of the new form is unified, covering both senior citizens and others under one system.

Form 15H vs Form 121 — What's Different?

|

Point

|

Form 15H (Old)

|

Form 121 (Current from April 2026)

|

|

Status

|

Earlier form for senior citizens

|

Active replacement from 1 April 2026

|

|

Who files

|

Resident individuals aged 60+

|

All eligible declarants under new unified system

|

|

Main use

|

Avoid TDS on interest & eligible income

|

Same purpose, unified structure

|

|

PAN

|

Mandatory

|

Still required under updated compliance

|

|

Validity

|

One financial year

|

New filing rules apply

|

The 15 g 15 h split — one form for under-60, one for senior citizens — no longer exists. Form 121 consolidates both.

Form 15G vs Form 15H — The Old Difference, for Context

For anyone who still wants to understand the difference between the two old forms:

Form 15G was for resident individuals aged 60 or below, and HUFs. The 15 g form epf and similar variations were used for bank interest, PF withdrawals, and other income.

Form 15H was for resident individuals aged 60 and above — senior citizens only. The 15 g 15 h system existed side by side, with the age cutoff being the key dividing line.

Both are now replaced by Form 121. But if you're researching old filings, refund claims, or helping an older family member understand their past declarations — the distinction still matters for those years.

Do You Still Need to Download Form 15H?

If you're looking for a 15h form download for Tax Year 2025–26 or earlier — yes, it's still available on the Income Tax Department's official website under "Income Tax Forms." That's valid for past years.

But for 2026–27 onwards? You need Form 121. Don't submit the old 15H for the current year — it won't be accepted under the updated system.

The download form 15 h option is still useful if you're handling returns or refunds for past years. Just know which year you're filing for before you download anything.

A Quick Note on the 15g and 15h Form Together

Many people used both forms within a family — a parent above 60 submitting 15H, a working adult below 60 submitting 15G. The 15g and 15h form pair covered most household scenarios.

Under the new system, all of that is handled through Form 121. One form, same purpose, simpler structure — at least in theory. Whether that makes things easier in practice remains to be seen.

FAQs

Q: Is Form 15H still valid in 2026?

A: No. From 1st April 2026, Form 15H has been replaced by the new unified Form 121 under the Income Tax Rules 2026. If you're filing a TDS declaration for Tax Year 2026–27 or later, you need to use Form 121 instead. Form 15H remains relevant only for past financial years.

Q: What is the difference between Form 15G and Form 15H?

A: Form 15G was for resident individuals aged 60 or below (and HUFs), while Form 15H was for senior citizens aged 60 and above. Both served the same purpose — preventing TDS deduction when the taxpayer's estimated income was below the taxable limit. From April 2026, both have been replaced by Form 121.

Q: Can a senior citizen use Form 15G instead of Form 15H?

A: No — the old system required senior citizens to use Form 15H, not Form 15G. The 15 g form was specifically for individuals below 60. However, since both have been replaced by Form 121 from April 2026, the age-based distinction no longer applies under the current system.

Q: Where can I download Form 15H for previous financial years?

A: The 15h form download is available on the official Income Tax Department website at incometax.gov.in under "Income Tax Forms." This is useful if you're dealing with returns, refunds, or declarations from Tax Year 2025–26 or earlier. Do not use the old form for current-year filings.

Q: What happens if I submitted Form 15H in 2025–26 — does it affect my 2026–27 filing?

A: No. Form 15H was valid only for the financial year it was submitted. For 2026–27, you need to submit a fresh declaration using Form 121. The old 15h submission does not carry forward and does not substitute for the new requirement.

Q: Is PAN mandatory for Form 15H or Form 121?

A: Yes — PAN was mandatory under the old 15h form and remains required under Form 121. Without a valid PAN linked to your declaration, the form is considered invalid and TDS will be deducted by the payer regardless of your income level.

Q: Can Form 15H be submitted online through SBI or other banks?

A: Yes, the 15 g form SBI and 15H were both available for online submission through SBI's net banking portal, as well as many other major banks. For current declarations under Form 121, check whether your bank has updated its online portal to accept the new form — not all platforms updated simultaneously after the April 2026 changeover.

Q: Do I need to submit Form 15H to every bank separately?

A: Yes — under the old system, a separate declaration was required for each deductor. If you had fixed deposits in three different banks, you'd submit the 15gh form to all three individually. The same principle likely applies under Form 121 as well, though the unified format simplifies the declaration itself.

Q: What income types does Form 15H cover?

A: Form 15H covered TDS on bank FD and RD interest, post office deposit interest, dividend income, EPF withdrawals (for those 60+), and other specified income payments. The 15 g form epf version covered PF withdrawals for those under 60. Form 121 now covers all these income categories under a single unified declaration.

Q: Can NRIs use Form 15H to avoid TDS?

A: No. Form 15H was strictly for resident individuals — NRIs were not eligible. The same restriction applies under Form 121. NRI income is subject to different TDS provisions under the Income Tax Act, and self-declaration forms like 15H or Form 121 do not apply to them.