If you're looking to save tax and grow your money at the same time, ELSS is probably the most efficient option under Section 80C. No other tax-saving instrument gives you equity exposure with a lock-in as short as three years. That combination is hard to beat.

Here's everything you need to know — what ELSS is, how the calculator works for both SIP and lump sum, how gains are taxed, and which funds have actually delivered strong returns.

What Is ELSS (Equity Linked Savings Scheme)?

ELSS — Equity Linked Savings Scheme — is an open-ended equity mutual fund that qualifies for tax deductions under Section 80C of the Income Tax Act, 1961. It's the only category of mutual funds that comes with built-in tax benefits.

By investing in an ELSS mutual fund, you can claim a deduction of up to ₹1,50,000 per year — which directly reduces your taxable income.

The portfolio of an ELSS scheme is diversified across equity-linked securities of companies across different market capitalisations and sectors. A smaller portion is typically invested in fixed-income securities as well. So you're not putting all your eggs in one basket — you get a diversified portfolio with a single investment.

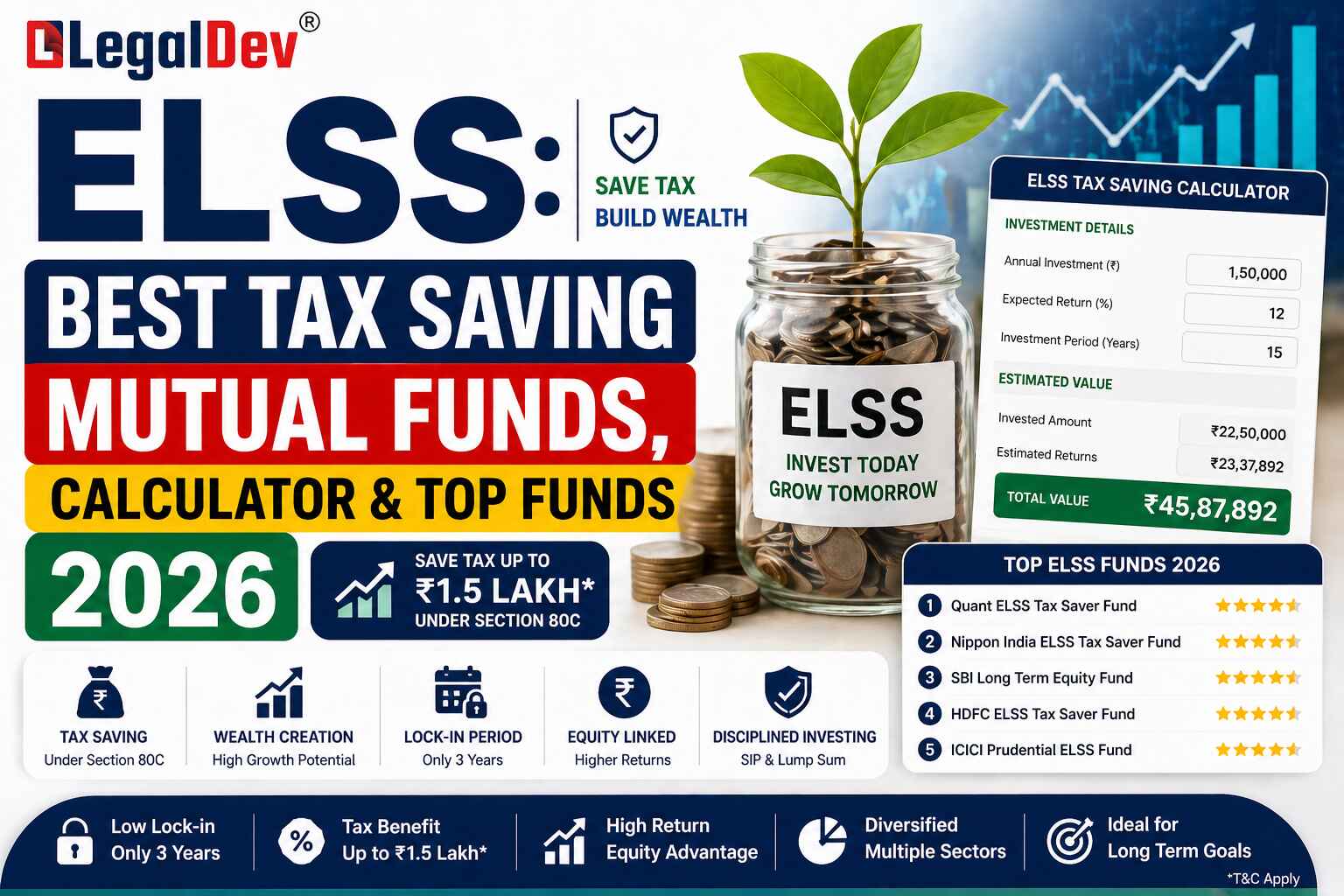

What Is an ELSS Calculator and How Does It Help?

An ELSS calculator is a simulation tool that estimates the future value of your investment based on the inputs you provide. To use it, you enter:

-

Mode of investment — SIP or lump sum

-

Investment amount

-

Frequency of investment (for SIP)

-

Expected annual rate of return

-

Duration of investment

Once you fill in these details, the calculator shows the estimated corpus your investment would have grown to by the end of the tenure. It's a useful way to align your investment amount with a specific financial goal.

If you want to reach a target faster, the ELSS calculator can also help you work backwards — showing you how much more you'd need to invest to hit your goal amount.

ELSS Calculator: SIP Mode

Systematic investing through SIP has become the go-to method for most mutual fund investors — and for good reason. Small, regular investments over time help you avoid the risk of putting a large sum in at the wrong market point. It also brings the benefit of rupee cost averaging.

For tax saving SIP specifically, an ELSS SIP calculator helps you estimate what your monthly investment will be worth at the end of the tenure. You enter the monthly amount, tenure, and expected rate of return — and the calculator gives you the maturity value.

SIP Example

Say you invest ₹5,000 per month for 12 months, with an expected return of 15% per annum.

-

Cumulative investment: ₹60,000 (₹5,000 × 12 months)

-

Estimated maturity value: ₹65,106

That said, this is an estimate. Factors like inflation, actual market performance, and tax implications aren't built into the calculator. Use it to get a directional sense of your investment — not as a guaranteed outcome.

ELSS Calculator: Lump Sum Mode

If you're investing a one-time amount rather than a monthly SIP, the lump sum version of the ELSS calculator works differently. You enter the total investment amount, the tenure, and an annualised rate of return — and it tells you what that investment would be worth at maturity.

Lump Sum Example

If you invest ₹50,000 in a tax saving mutual fund for 60 months at an annualised return of 15%, the estimated maturity value comes out to approximately ₹1,00,568.

One thing to keep in mind: the lock-in period for all ELSS funds is a minimum of three years from the date of purchase. You can't redeem before that, regardless of market conditions. And just like the SIP calculator, the lump sum version doesn't account for taxes or real-world market volatility in its output.

How Are ELSS Funds Taxed?

Capital gains from ELSS mutual funds are taxable — but the structure is reasonably investor-friendly.

Since the lock-in period is three years, any gains you realise are treated as Long-Term Capital Gains (LTCG). The first ₹1,25,000 of LTCG in a financial year is tax-exempt. Any gains beyond this limit are taxed at 12.5%, and there's no indexation benefit available.

Dividends, if you opt for that payout option, are taxed differently. They're added to your total income and taxed at your applicable income tax slab rate. This changed with Budget 2020 — prior to that, dividends were tax-free in investors' hands since companies were paying Dividend Distribution Tax (DDT).

So for most investors going the ELSS tax saving route, the growth option is more efficient from a tax standpoint.

Top Rated ELSS Funds: Best Performers Across AMCs (Past 3-Year Returns)

Past returns don't guarantee future performance. That caveat matters, and it's worth saying upfront. But looking at top ranked ELSS funds over a 3-year horizon does give you a sense of consistency and fund manager capability.

Here are the top 10 ELSS funds based on annualised returns across 1-year, 3-year, and 5-year periods:

|

Fund Name

|

1Y Annualised (%)

|

3Y Annualised (%)

|

5Y Annualised (%)

|

|

HDFC ELSS Tax Saver

|

14.74

|

21.18

|

20.72

|

|

Motilal Oswal ELSS Tax Saver Fund

|

16.59

|

20.66

|

19.66

|

|

ITI ELSS Tax Saver Fund

|

8.73

|

18.25

|

17.09

|

|

JM Tax Gain Fund

|

15.83

|

17.80

|

19.64

|

|

Parag Parikh ELSS Tax Saver Fund

|

13.92

|

17.47

|

23.05

|

|

Quantum ELSS Tax Saver Fund

|

15.29

|

17.42

|

18.50

|

|

DSP Tax Saver MF

|

15.32

|

16.99

|

20.13

|

|

Franklin India ELSS Tax Saver Fund

|

12.02

|

16.98

|

19.43

|

|

Taurus ELSS Tax Saver Fund

|

9.58

|

16.74

|

16.65

|

|

HSBC ELSS Tax Saver Fund

|

15.95

|

16.07

|

16.90

|

|

Bank of India ELSS Tax Saver Fund

|

2.77

|

15.62

|

20.66

|

A few things stand out here. The HDFC tax saving fund leads on 3-year returns. Parag Parikh leads the pack on 5-year annualised returns at 23.05% — impressive consistency. DSP Tax Saver MF and Axis ELSS Tax Saver Fund (not shown above but widely tracked) are among the most consistently recommended by advisors for good ELSS funds over the medium term.

The SBI ELSS Tax Saver Fund and Axis Long Term Equity Fund also feature in most recommended ELSS funds lists, particularly for investors who prefer large-cap heavy portfolios with lower volatility within the equity linked scheme category.

Which Is the Best ELSS Mutual Fund to Invest In?

There's no universal answer — and anyone who gives you one without knowing your goals, horizon, and risk tolerance is oversimplifying.

That said, some filters that typically work for identifying best ELSS mf options:

-

Consistent 3-year and 5-year annualised returns across market cycles

-

Experienced fund management team

-

Reasonable expense ratio

-

Portfolio diversification across market caps

For top rated ELSS mutual funds in the current environment, the names above — HDFC, Parag Parikh, Motilal Oswal, and DSP — tend to appear on most shortlists. But please cross-check with your registered financial advisor before making any ELSS investment decision.

Why ELSS Is One of the Best Tax Saving Investments Under 80C

Compared to other Section 80C options — PPF (15-year lock-in), NSC (5-year), or traditional insurance plans (almost always a bad idea purely for tax saving) — ELSS saving scheme stands out for a few clear reasons:

-

Shortest lock-in — just 3 years

-

Highest return potential — equity exposure gives it a clear edge over debt-linked 80C instruments

-

Flexible investment — SIP or lump sum, your choice

-

Dual benefit — tax saving today + wealth creation over time

The equity linked saving route does come with market risk, which the others don't. But for a 3-year-plus horizon, most top elss funds have historically delivered better returns than fixed-income alternatives.

Disclaimer: The fund performance data is sourced from AMFI, Morningstar Research, and Ace MF and is meant for educational purposes only. Past returns do not guarantee future performance. Please consult your SEBI-registered financial advisor before making any investment decision.

FAQs

Q: What is the lock-in period for ELSS mutual funds?

A: The minimum lock-in period for all ELSS funds is 3 years from the date of purchase — or from each SIP instalment date, if you're investing via SIP. You cannot withdraw or redeem before this period, regardless of market conditions. After 3 years, your investment becomes freely redeemable.

Q: Which is the best ELSS mutual fund to invest in for 2026?

A: Based on 3-year and 5-year annualised returns, HDFC ELSS Tax Saver, Parag Parikh ELSS Tax Saver Fund, and Motilal Oswal ELSS Tax Saver Fund have consistently featured among the top ranked ELSS funds. DSP Tax Saver MF and Axis Long Term Equity Fund are also widely recommended. That said, the best ELSS mutual fund for you depends on your risk profile, goals, and time horizon — always check with a registered advisor.

Q: How much tax can I save by investing in ELSS?

A: Investing in an equity linked savings scheme allows you to claim a deduction of up to ₹1,50,000 under Section 80C of the Income Tax Act. The actual tax saved depends on your income tax slab — for someone in the 30% bracket, that's up to ₹46,800 in tax savings annually. ELSS is the only mutual fund category that qualifies for this deduction.

Q: How is the ELSS calculator useful — and what are its limitations?

A: An ELSS calculator helps you estimate the future value of your investment based on the amount, tenure, and expected rate of return — for both SIP and lump sum modes. It's useful for planning and goal-setting. But it's an estimate, not a guarantee — actual returns depend on market performance, which the calculator doesn't factor in. Treat the output as a directional input, not a fixed number.

Q: Are ELSS gains fully tax-free?

A: Not entirely. Since ELSS funds have a 3-year lock-in, all gains are treated as Long-Term Capital Gains (LTCG). The first ₹1,25,000 of LTCG per financial year is exempt from tax. Any gains above this are taxed at 12.5% with no indexation benefit. Dividends, if opted for, are taxed at your applicable income slab rate. So ELSS tax saving works both at the investment stage (80C deduction) and partially at the gains stage (LTCG exemption up to ₹1.25 lakh).

Q: Can I invest in multiple ELSS funds at the same time?

A: Yes, you can invest in multiple ELSS mutual funds simultaneously. However, the total Section 80C deduction is capped at ₹1,50,000 across all investments combined — not per fund. So spreading your elss investment across two or three top rated ELSS funds is fine for diversification, but it doesn't increase your tax deduction limit.

Q: Is SIP better than lump sum for ELSS investment?

A: For most salaried investors, tax saving SIP is the more practical route — it spreads the investment across the year and helps with rupee cost averaging. A lump sum works better if you have a surplus at year-end and want to maximise the 80C benefit quickly. Both modes have the same 3-year lock-in per instalment, but SIP gives you more flexibility in managing market timing risk across the elss saving scheme.

Q: What happens to my ELSS investment after 3 years?

A: After the 3-year lock-in period, your ELSS mf investment becomes liquid — you can redeem it partially or fully at any time. There's no compulsion to withdraw at exactly 3 years. Many investors choose to stay invested longer, since equity-linked schemes tend to reward patience. Redeeming only when you actually need the money is generally the smarter approach.

Q: Can I start ELSS SIP with a small amount?

A: Yes. Most elss funds allow SIP investments starting from ₹500 per month. This makes elss investment accessible even for first-time investors or those just starting their tax-saving journey. The ELSS SIP calculator can help you figure out how much to invest monthly to reach a specific corpus target over your preferred tenure.

Q: What is the difference between ELSS and PPF for tax saving?

A: Both ELSS and PPF qualify for Section 80C deduction up to ₹1,50,000. The key differences: PPF has a 15-year lock-in versus ELSS's 3 years. PPF currently offers around 7.1% returns (fixed, debt-linked), while top elss funds have historically delivered 15–20%+ over 5-year periods (equity-linked, market-dependent). ELSS carries higher risk but offers meaningfully higher return potential. For long-term wealth creation alongside tax saving, ELSS generally wins — but for capital safety, PPF has its place.