CTC in Salary: Full Form, Meaning, Structure, Examples, and How to Calculate It

Update (April 2026): From April 1, 2026, the Code on Wages 2019 has been officially implemented. Under the new rules, basic salary must now constitute at least 50% of total CTC — which directly impacts EPF deductions and your monthly in-hand salary. This affects every salaried employee in India. Details added in the relevant section below.

Everyone has come across the word CTC. Peers mention it, relatives ask about it, job offers are thrown around using it. But most people never actually sit down and understand what it means for their pocket.

The full form of CTC in salary is Cost to Company — the total amount a company spends on an employee for their services. This includes salary, benefits, bonuses, and any other related expenses. Understanding CTC matters because it directly shapes how you read your own compensation structure.

What Is CTC in Salary?

The Cost to Company (CTC) is the total cost an employer incurs to hire and retain an employee for a year. That includes salary, benefits, allowances, bonuses, provident fund contributions, and everything else. In other words, CTC is every rupee the company spends because of you.

But here is the part most people miss. CTC is not the amount that lands in your bank. Various deductions and contributions are removed from the CTC before you arrive at your actual take-home salary.

Actually — let me put it more plainly. The company's number and your number are never the same.

Not sure how to handle GST? Let our experts do it for you.

✔ Fast process ✔ 100% online ✔ Expert support

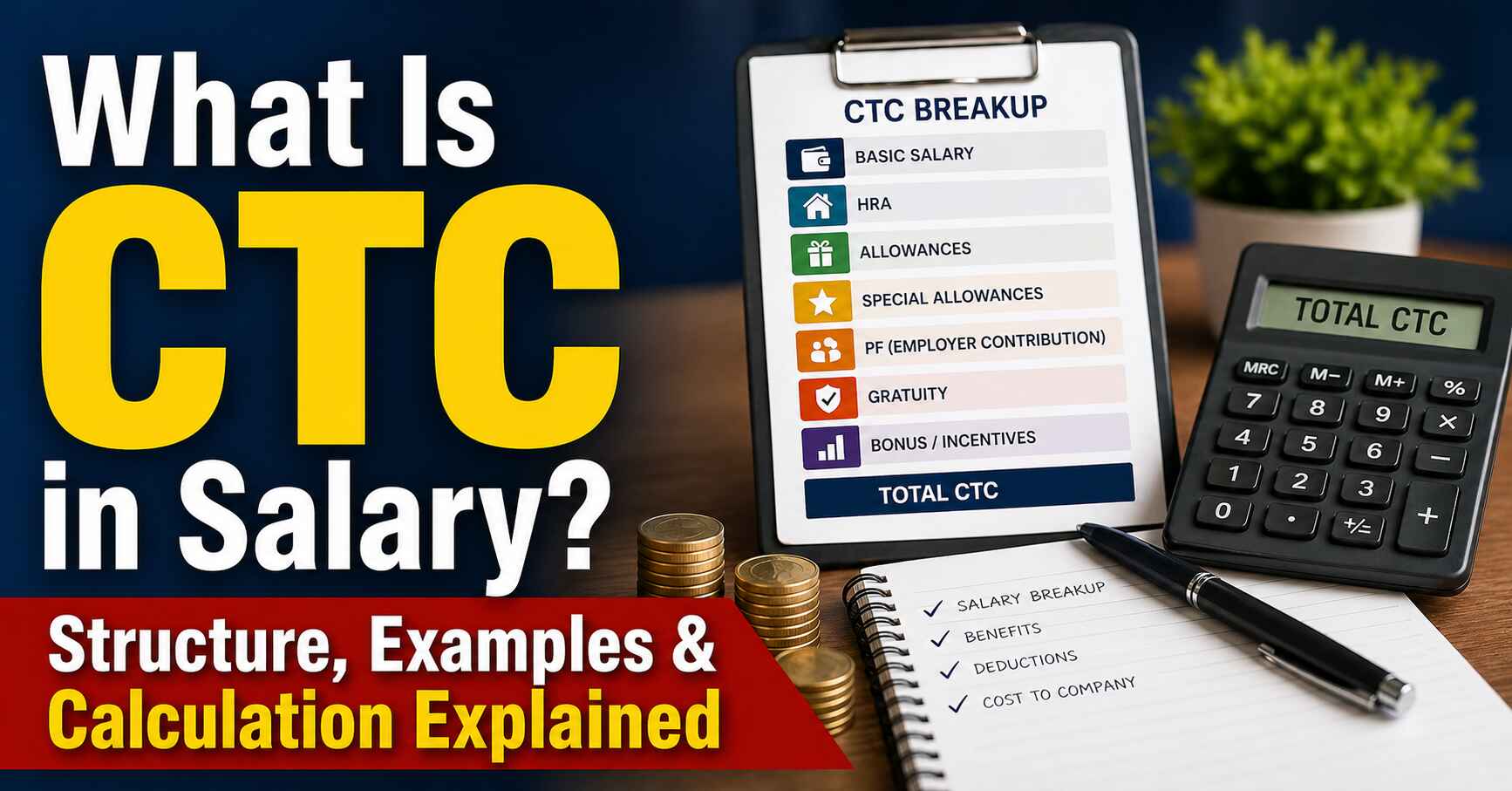

Structure and Key Components of CTC

Your CTC has several components — salary, benefits, allowances, and bonuses. Here is what is actually included.

Fixed Components

Basic Salary This is the base salary an employee earns, excluding all allowances and bonuses. It is also the figure from which most other calculations — EPF, HRA, gratuity — are derived.

Update (April 2026): Under the Code on Wages 2019, now effective from April 1, 2026, basic salary must be at least 50% of total CTC. Many companies previously kept it as low as 25–40% to minimize EPF and gratuity obligations. That practice ends now. The impact: higher EPF deductions, better long-term savings, but a slightly lower monthly in-hand for most employees.

Dearness Allowance Dearness Allowance is given as an adjustment to the cost of living, aimed at countering inflation. It applies primarily to government employees.

House Rent Allowance HRA covers the employee's housing costs and is tax-deductible for those living in rented accommodation.

Variable and Performance-Linked Components

Performance Bonus This is the payment given based on the employee's performance for the year.

Sales Commission An incentive paid to sales representatives based on the revenue they generate monthly.

Profit Sharing Distribution of a portion of the company's profits among employees.

Other Benefits

Provident Fund A retirement benefit where both employer and employee contribute a percentage of basic salary every month. Both contributions form part of the CTC.

Health Insurance Some employers offer health insurance covering medical expenses for the employee and their family. The premium paid by the employer is included in the CTC.

Medical Allowance An amount paid to cover day-to-day medical expenses.

Deductions from CTC

Professional Tax Deducted depending on the state of employment.

Income Tax Based on applicable income tax slabs and estimated tax liability, a certain amount is deducted as Tax Deducted at Source (TDS). For FY 2025-26, salaried individuals under the new tax regime get a standard deduction of ₹75,000 — making income up to ₹12.75 lakh effectively tax-free.

Other Contributions All employee contributions towards PF, NPS, and similar instruments are deducted from CTC.

Not sure how to handle GST? Let our experts do it for you.

✔ Fast process ✔ 100% online ✔ Expert support

How to Calculate CTC in Salary

CTC is the total cost the employer has to incur — every expense towards an employee, added up.

CTC = Gross Salary + Benefits + Other Costs

For example: if Gross Salary is ₹5 lakhs, PF contribution is ₹80,000, and Bonus is ₹20,000, the CTC works out to ₹6 lakhs (₹5,00,000 + ₹80,000 + ₹20,000).

Simple enough. But how does this translate to what you actually take home?

CTC Format and Example

Let's work through a real example.

Mr. Anban is a Manager at ABC Pvt. Ltd. He gets a basic salary of ₹15 lakhs, HRA of ₹2 lakhs, allowances of ₹50,000, a performance bonus of ₹1.5 lakhs, and makes an EPF contribution of ₹2 lakhs. His total CTC breaks down like this:

|

Particulars |

Amount (₹) |

|

Basic Salary |

15,00,000 |

|

HRA |

2,00,000 |

|

Allowances |

50,000 |

|

Performance Bonus |

1,50,000 |

|

EPF Contribution |

2,00,000 |

|

CTC |

21,00,000 |

So Mr. Anban's CTC for the year is ₹21 lakhs. But that is not his in-hand salary. Not even close.

CTC vs Gross Salary vs In-Hand Salary

To find Mr. Anban's actual in-hand salary, we first calculate his Gross Salary:

|

Particulars |

Amount (₹) |

|

Basic Salary |

15,00,000 |

|

HRA |

2,00,000 |

|

Allowances |

50,000 |

|

Performance Bonus |

1,50,000 |

|

Gross Salary |

19,00,000 |

Now the tax part. Under the new tax regime for FY 2025-26, his tax liability works out to ₹2,14,500.

Use our Income Tax Calculator to check your exact tax liability.

So his in-hand salary looks like this:

|

Particulars |

Amount (₹) |

|

CTC |

21,00,000 |

|

(–) EPF Contribution |

–2,00,000 |

|

Gross Salary |

19,00,000 |

|

(–) Tax Liability |

–2,14,500 |

|

In-Hand Yearly |

16,85,500 |

|

In-Hand Monthly |

1,40,458 |

Now — what if Mr. Anban reduces his EPF contribution to ₹1 lakh?

|

Particulars |

Amount (₹) |

|

CTC |

21,00,000 |

|

(–) EPF Contribution |

–1,00,000 |

|

Gross Salary |

20,00,000 |

|

(–) Tax Liability |

–2,14,500 |

|

In-Hand Yearly |

17,85,500 |

|

In-Hand Monthly |

1,48,792 |

The CTC does not change. But the monthly in-hand goes up by over ₹8,000. That is the direct impact of managing your contributions.

And that is worth knowing before you sign anything.

Final Word

Planning deductions and contributions from CTC is not optional — it matters. A higher contribution means a lower in-hand. A lower contribution means more in your pocket today, but less saved for the future. It depends entirely on the employee's financial situation and goals.

But the starting point is this: understand how your CTC is structured. Once you do, you can actually plan — instead of just waiting for what shows up in your account every month.

⑩ 5 FAQs

Q: How to calculate in-hand salary from CTC? A: Subtract all contributions (EPF, NPS, etc.) and employer-side components from CTC to arrive at Gross Salary. Then deduct your tax liability (TDS) and professional tax from Gross Salary. Whatever remains is your in-hand or take-home salary. The exact amount varies based on your contribution choices and tax regime.

Q: What is the difference between CTC and in-hand salary? A: CTC is the total annual cost the company bears for you — including EPF, gratuity, insurance, and all benefits. In-hand salary is what actually reaches your bank account after all deductions. For most salaried employees in India, in-hand can be 20–35% lower than the CTC figure.

Q: Is CTC monthly or yearly? A: CTC is a yearly figure. It represents the total cost incurred by the employer over a full year. When companies quote CTC during hiring, they always mean the annual number — not monthly.

Q: Does a higher CTC always mean a higher in-hand salary? A: Not always. Two employees with the same CTC can have very different in-hand amounts depending on variable pay structure, EPF contribution levels, tax regime chosen, and employer-side benefits like gratuity and insurance. A ₹15 LPA offer with 25% variable pay will often result in a lower monthly in-hand than a ₹13 LPA fully fixed offer.

Q: What is the impact of the new Code on Wages 2019 on CTC structure? A: From April 2026, basic salary must be at least 50% of total CTC under the Code on Wages 2019. This means higher EPF deductions (since EPF is calculated on basic), better long-term retirement savings, but a slightly lower monthly in-hand for many employees. Total CTC remains unchanged — only the internal distribution of components shifts.